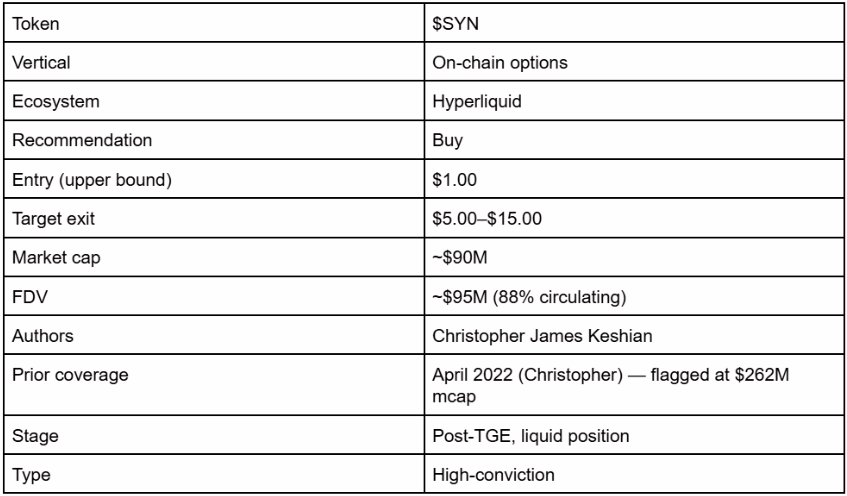

On rare occasions, we like to publish some of our highest conviction investments as public write-ups for our readers. This past week, Triton began to acquire a position in Hypercall ($SYN).

Original publication date June 25, 2026 | Price ~$0.40 | Market cap ~$90M

Synapse Protocol, a five-year-old multichain bridging project, has pivoted to Hypercall, a permissionless on-chain options protocol built on Hyperliquid. The founder has wound the bridging business down on purpose and said so directly. Hypercall is now the whole company.

At roughly $90M market cap, $SYN is priced like the bridge failure is the only thing that matters and Hypercall barely exists. We don't think that's right. On-chain options is the most under-built derivatives market in crypto, and every prior attempt at it failed for the same fixable reason: no deep on-venue perps market to hedge delta against. Hyperliquid fixes that. Hypercall is live on Mainnet Alpha as of June 2026.

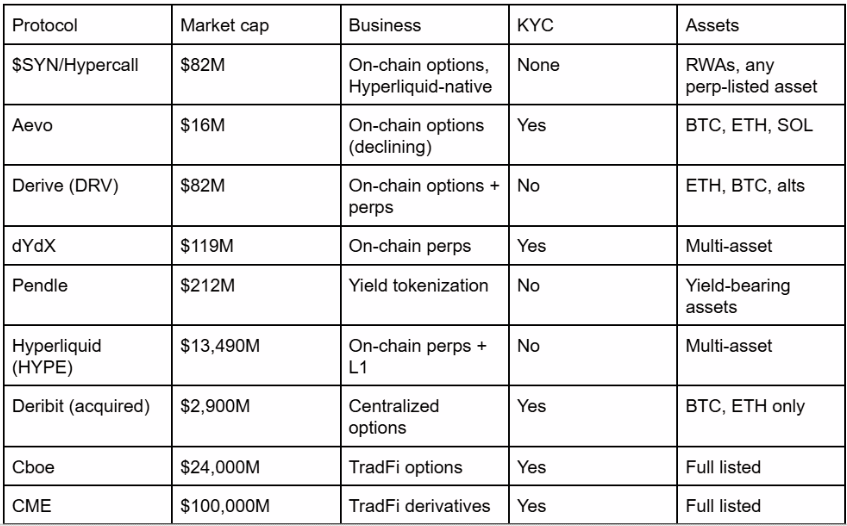

The comp gap is the anchor here. Coinbase paid $2.9B for Deribit, which lists seven assets behind KYC. Hypercall, at $90M, can list options on any tokenized asset with no KYC, and SpaceX options are already trading.

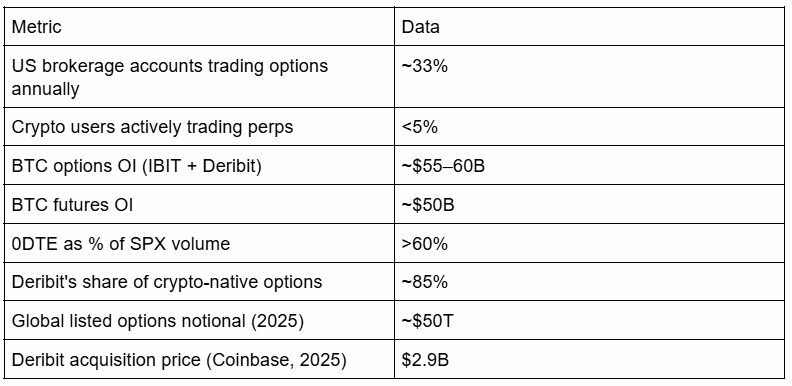

Options are the most widely traded derivative in the world by notional. The global listed options market cleared about $50 trillion in notional in 2025, a sixth straight record year. About a third of US brokerage accounts trade options at least once a year. 0DTE contracts, options expiring the same day they're traded, now make up more than 60% of SPX volume, and retail trades them in size on Robinhood.

Crypto looks nothing like that. Fewer than 5% of crypto users trade perps, let alone options. Deribit holds about 85% of the crypto-native options market and lists seven assets. That gap, between what exists on-chain and what retail demand would support, is the whole thesis.

The 0DTE number is worth sitting with: the most complicated options product that exists is now the highest-volume instrument in the world's most liquid equity options market, and retail figured it out on Robinhood with no finance background. The barrier was never the complexity of the instrument. It was venue quality and UX.

Every prior DeFi options project, Lyra, Aevo, Dopex, Derive, had legitimate teams and real capital, and none of them got traction. The usual explanation is that options are too complicated for retail. That's not what happened. The problem is structural, and it comes down to how market makers operate.

Picture a market maker trying to quote a three-month BTC call on a standalone DeFi options venue. They post collateral on the options platform. To hedge delta, they need to short BTC, but there's no deep perps market on that same platform, or if there is, it's thin with wide spreads. So they hedge off-venue, on Bybit or Binance Futures or dYdX. Now their capital is split across two systems: options margin in one place, hedge capital in another. Every time spot moves they're rebalancing both accounts, watching two liquidation thresholds, paying funding on the hedge, and eating basis risk between venues.

That raises their effective cost of capital, so they widen spreads to stay profitable. Wide spreads mean bad fills for takers, bad fills mean less taker flow, and less taker flow means market makers pull back further. The venue never gets the depth it needs, and the spiral runs the wrong way.

The founder put it well: options are "10x harder to bootstrap than perps." Not a product problem, not a marketing problem. A capital efficiency problem with no real fix on a venue that doesn't have native perps.

Hypercall's answer: options writers hedge delta directly in Hyperliquid's own perps, in the same margin account as the options position. One account, one margin pool, one liquidation framework. Cheaper hedging means tighter spreads, tighter spreads pull in more takers, more takers balance the book, and the venue compounds from there instead of stalling.

Hypercall is permissionless, built directly on Hyperliquid, with options and their perp hedges sharing one margin account.

As of June 2026: Mainnet Alpha is live, USDC deposits and withdrawals work, and SpaceX options trade with 0DTE and daily expiries that NASDAQ doesn't offer. Portfolio margining is launching soon, which should let institutional market makers post Hyperliquid perp positions as collateral and lift the OI cap. Builder-code revenue sharing is live; referrals are coming.

Through TradeXYZ and similar tokenization protocols on Hyperliquid, Hypercall can list options on any tokenized asset: private equity, commodities, crypto. No prior on-chain venue could do that.

SpaceX is the proof of concept. SPCX 0DTE options are live; NASDAQ only offers weekly and monthly expiries on the name. When Hyperliquid lists pre-IPO perps for companies like Anthropic or OpenAI, Hypercall will likely be the only place to trade options on them for a while.

One data point from alpha: $20,000 in 0DTE SPCX premiums generated over $15M in hedging orderflow on the SPCX perp. The loop between options volume and perp demand is already showing up at alpha scale.

The mechanics matter here, and the clearest example is the most famous retail trade in crypto's short history. When Roaring Kitty spotted the GameStop mispricing in 2019, he built his position in $8 calls, paying about $0.50 in premium each. Max loss was the premium. A $10,000 stake returned roughly $7.7M.

Run the same trade with 3x long perps: entry $5, liquidation at $3.33. GameStop touched $3.00 in March 2020 on its way to $325. The perp position gets liquidated on day 301, directionally right, fully wiped out anyway. Even 2x leverage doesn't survive long enough.

That's the case for options on volatile, long-duration trades: the downside is fixed at entry. No funding to watch, no margin calls, no liquidation while you wait for the thesis to play out. It's also why a third of US brokerage accounts trade options annually while fewer than 5% of crypto users touch perps: the better instrument for this kind of trade just hasn't existed on-chain yet.

Options venues build stronger network effects than almost anything else in finance, for a mechanical reason: collateral lock-in. A market maker who sells a six-month call keeps margin posted on that exchange for the life of the option. New strikes and expiries pile more margin onto the same venue. Unwinding means closing or rolling dozens of positions across strikes and expiries, each with its own spread cost. Switching gets more expensive with every listing cycle.

Deribit lists seven assets and isn't, by most accounts, a particularly pleasant product to use: no retail UX, limited strikes and expiries, KYC that locks out a lot of the world. Binance and OKX, with far bigger balance sheets and distribution, have tried for years to take share from Deribit and failed. The lock-in held anyway.

Hypercall can build the same kind of lock-in, starting from Hyperliquid's hundreds of listed assets instead of Deribit's seven. That's the TAM expansion, in short.

The flywheel: market makers hedge delta in Hyperliquid perps, which creates real trading activity in the underlying. That demand supports further-out strikes and wing options, spreads tighten, more takers show up, flow balances, more assets and expiries get listed, capital deepens, switching costs climb. It's the same gravity that built Deribit, except here it starts from Hyperliquid's existing liquidity instead of zero.

Synapse launched in 2021 as a multichain bridge. It moved over $55B cumulative volume across 25 chains, served 2 million addresses, and was built by a team of three to five people with no VC money. It never had a major security incident, notable in a space where LayerZero lost $300M and Nomad lost $700M.

The bridge business is now deliberately on the back burner. In his June 2026 post-mortem, the founder says plainly that after four years in bridging, the team decided a structurally profitable bridging business doesn't exist. Stargate, backed by over $300M in institutional money, made about $65,000 in profit last quarter: millions of cross-chain messages for under $1,000 in revenue.

This wasn't a Synapse mistake. It hit the whole industry.

Security pressure forced three full rebuilds: SynChain (TSS validators), Optimistic Bridging (100,000 lines of Solidity/Go, two audits), then SYN v3, each triggered by new exploits elsewhere in the industry, where $2B was stolen by state actors in a single year, even though Synapse itself was never hit.

Liquidity deals were winner-take-all: lose one and a competitor could bridge for free against Synapse's slippage and emissions costs, so chasing these deals ate engineering time continuously.

And the team burned out. Three to five engineers processed tens of billions during the 2021 bull run, and the founder is candid in his post-mortem about how that burnout affected decision quality. That kind of honesty is rare, and we read it as a point in his favor, not against him.

Between bridging and Hypercall, the team also built Cortex, an AI-powered DeFi trading frontend, which launched into a weak market and got shelved. It's a fair thing to flag; see Risks below.

$SYN went from about $4.92 at its January 2021 peak to under $0.03 at the bottom, a 99% drawdown, and has recovered to about $0.40 on Hypercall momentum, still down roughly 93% from the old high. We see that drawdown as the opportunity: the bridge failure is already priced in, and Hypercall is getting close to zero credit at current levels.

Jake Sylvestre (@trajan0x), founder.

His public post-mortem on Synapse stands out. He takes direct responsibility for the post-2022 delays, names the specific structural causes (burnout, staffing), and walks through each architecture pivot with real technical detail. His April 2026 thread on options market structure shows he actually understands the space: he names options market maker cost of capital as the core constraint, gets the Deribit flywheel, separates institutional from retail options dynamics, and maps Hypercall against every known failure mode in prior DeFi options protocols.

Track record: $55B in cumulative bridge volume with a team of three to five and no VC, no major security incidents, and a willingness to actually kill low-margin products instead of keeping them alive for appearances.

Incentives: founder tokens are being re-locked, team compensation is milestone-linked (modeled on Tesla's 2018 pay package: the team gets nothing unless token holders do first), and there's no VC unlock overhang or preference stack to worry about.

$SYN is the single governance token across Synapse, Cortex, and Hypercall. CX (Cortex) is interchangeable with $SYN, so everything sits in one liquid token, listed on Binance and Kraken.

There's no equity here. All future cash flow runs through $SYN via the DAO.

Value accrual:

The key difference from earlier DeFi tokens: revenue goes to buybacks and market maker incentives instead of sitting in a treasury. With 88% circulating and no vesting cliffs left, there's no obvious wall of future sellers. The Bitget delisting was a minor exchange event; Binance's listing status is the thing that actually matters for liquidity.

Coinbase paying $2.9B for Deribit (seven assets, mandatory KYC, no on-chain architecture) and immediately announcing a push into equities options and tokenized stocks is about as direct a validation of Hypercall's product direction as you'll get. That price implies roughly 32x Hypercall's current market cap for a worse product addressing a smaller market.

Hyperliquid itself went from zero to over $900M in annualized profit in about 18 months, which gives a sense of how fast on-chain derivatives venues can scale once they find traction. Being native to that ecosystem means Hypercall inherits liquidity and attention no standalone options protocol has ever had.

Tokenized RWAs extend the addressable market further. SpaceX has no liquid, retail-accessible instrument anywhere in traditional markets outside high-minimum private secondary deals. SPCX options on Hypercall, permissionless, USDC-margined, non-custodial, 24/7, actually fill that gap. The real TAM isn't "crypto options users," it's anyone with a wallet who wants defined-risk exposure to private equity.

On the regulatory side, the pullback in aggressive SEC enforcement, plus the GENIUS and CLARITY Acts, has cleared up a lot of the legal ambiguity that used to scare off on-chain derivatives products for US users.

$SYN trades at $0.375, circulating market cap about $82M. A 10x gets you to roughly $3.75 and an $820M cap, between Pendle ($212M) and Hyperliquid ($13.5B) in the on-chain derivatives pecking order, and still well under the $2.9B Coinbase paid for Deribit. Whether 10x is plausible isn't really in question. What matters is what Hypercall actually has to do to get there.

$SYN trades at parity with Derive, a permissioned, institution-leaning options protocol, even though Hypercall beats it on every axis: no KYC, $1 fractional contracts, 24/7 global access, RWA-native markets, and a real perps hedge built in. At $82M, the market is pricing $SYN like Hypercall barely matters.

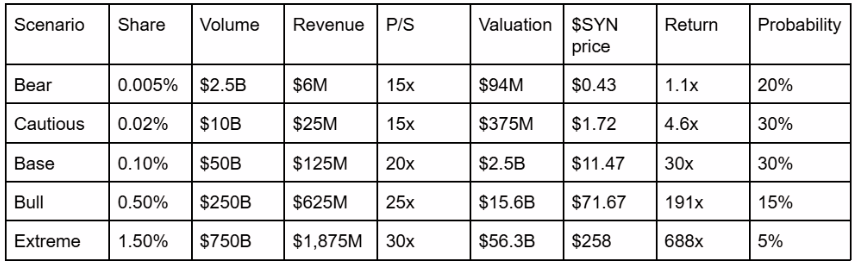

Bear assumes Hypercall gets some early traction but can't land credible market makers: volume stuck at $5–10M/day, the product works but liquidity is too thin to matter. $SYN re-rates a little. This is just where Phase 0 alpha leaves things if nothing else happens.

Cautious has Hypercall passing the entire current DeFi options market and becoming the default venue for permissionless crypto options: $10B/year, about $27M/day, roughly 10% of Deribit's current daily notional. Realistic within 12 months if portfolio margining ships clean and a couple of institutional market makers come on. Worth a clean 4–5x on its own.

Base puts Hypercall at $137M/day, around 5% of Deribit, but the mechanism is different. Hypercall isn't fighting Deribit for its existing users; it's reaching the billions of people Deribit can't serve because of KYC, geography, or contract minimums. At $11.47, the protocol's valued around the Deribit acquisition price, for a permissionless, multi-asset, 24/7 venue.

Bull has Hypercall running as a full options exchange across crypto, RWAs, equities, and commodities, with real institutional market makers and SPAN-style portfolio margining live: a two-to-three-year buildout that needs continued regulatory tailwinds and clean execution.

Extreme puts Hypercall among the top five options venues globally by notional, a five-to-ten-year scenario included to bound the distribution, not something we expect.

The probability-weighted EV comes to $27.69, about 74x current price. Treat that as a distribution parameter, not a target; it's sensitive to the tail scenarios. Halve the Bull and Extreme probabilities and EV still lands around $10, about 27x. What stands out is the asymmetry: Bear is roughly flat (1.1x) while Cautious alone is a clean 4–5x. The market isn't even pricing in Cautious.

A 10x return needs $3.75 and an $820M cap. Working backward through the model at 25bps fees and 20x P/S: that's $41M in annual revenue, $16.5B in annual volume, 0.033% of global options notional, about $45M/day.

Derive currently does $30–60M/day. So a 10x just requires Hypercall to match Derive's current run rate. That's a product execution question, not a moonshot.

Mainnet Alpha product risk: High. Hypercall hasn't shown sustained volume yet, hasn't cleared a real market structure test, and hasn't onboarded institutional market makers at scale. Every milestone is still ahead of it. OI caps are currently capping user activity until institutional MMs come on. This is the dependency to watch most closely right now.

Binance monitoring tag: Medium. Binance flagged $SYN for volatility on May 22, 2026, and Bitget delisted $SYN/USDT on June 18. A Binance delisting would hurt liquidity badly and make exiting any sizable position hard. Check this weekly; it's the most important external risk on the table.

Multi-pivot history: Medium. This is the team's third direction: bridge, then Cortex, then Hypercall. The fair critique is that 18-month crypto cycles push teams toward narrative-driven pivots, and that critique applies here too. The founder's post-mortem reads as credible: each pivot looks rationally motivated rather than opportunistic, but that's based on what he's disclosed, not anything we've verified independently. Worth watching how committed the team stays once Hypercall hits real friction.

Market maker bootstrapping: Medium. The founder calls options liquidity "10x harder than perps" to bootstrap, and no institutional market maker is publicly confirmed yet. Thin liquidity at launch could sour the user experience before the flywheel gets going. This risk eases once portfolio margining is live and a market maker is on record.

Recent price action: Medium. The token is up about 283% over the past week on narrative, well ahead of actual product traction. Real risk of reversion here, and this isn't a stable base to size into.

Token dilution: Low. 88% issued, no VC vesting cliffs left. About as clean as DeFi tokenomics get at this market cap.

The model's Bear scenario (1.1x, basically flat) isn't designed to be a disaster. Actual total loss needs one of: regulators shutting down permissionless on-chain derivatives somewhere major, a smart contract exploit, Hyperliquid losing its dominant position, or the DAO failing to actually formalize fee-to-buyback, leaving $SYN as pure narrative with nothing backing it. That last one is the most likely and the one worth watching most; the upcoming DAO vote on the buyback mechanism is the signal to track.

Buy | Entry up to $1.00 | Target $5–$15

At roughly $90M market cap, $SYN offers asymmetric exposure to a real thesis: on-chain options is the biggest under-built derivatives market in crypto. The bear case, bridging collapsing, has already played out and is baked into a 92% drawdown from the prior cycle high. The bull case, Hypercall becoming the leading permissionless on-chain options exchange on Hyperliquid, has a realistic path to $300–800M market cap, a 10x to 25x return from here.

Why we like it: the team has no VC, no new token, founder tokens being re-locked, and compensation tied to milestones. Those incentives actually point at token holder value instead of team liquidity. The structural insight behind Hypercall is right: on-chain options should be a multi-billion-dollar market, and the thing that killed every prior attempt, capital split between options and hedging venues, is solved by building on Hyperliquid. Coinbase's $2.9B Deribit purchase backs this up institutionally, at a price implying a 32x comp gap to current $SYN.

The price is discounting failure almost entirely. At $90M, the market is pricing close to zero odds that Hypercall works. Getting to 10% of Deribit's acquisition value only takes Derive-level daily volume: an execution milestone, not a market-capture fantasy. And the timing lines up: Mainnet Alpha is live right as the Coinbase/Deribit deal, tokenized equity growth, and Hyperliquid's own momentum are all peaking at once.

What we're watching before scaling the position further:

Prior writeup: Christopher James Keshian, April 2022. This writeup started June 21, 2026.

On rare occasions, we publish our highest-conviction investments. This week, Triton initiated a position in Hypercall (SYN). Our view: the market is pricing its past, while overlooking Hypercall's potential as a leading on-chain options platform.

Triton fully exited liquid assets by June 3 as macro pressure, ETF outflows, weak market structure, and capital rotation turned crypto risk-reward negative. The decision was not driven by broken fundamentals, but by a market where downside risk outweighed upside until clearer re-entry signals emerge.

We see Q1 2026 as a rare asymmetric crypto entry point—fundamentals are intact, valuations reset, and sentiment is at multi-year lows—positioning our long-horizon capital to capture potential outsized returns through our vertical-focused, data-driven approach.