This is not financial advice. Anything stated in this article is for informational purposes only and should not be relied upon as a basis for investment decisions. Triton may maintain positions in any of the assets or projects discussed on this website. Triton Limited is incorporated in the Abu Dhabi Global Market (“ADGM”) and is regulated by the Financial Services Regulatory Authority (“FSRA”) under Financial Services Permission number 240017.

TL;DR

Triton fully exited liquid assets by June 3 because risk-reward turned negative, not because fundamentals broke.

Major crypto assets broke key levels on June 2 as institutional ETF outflows accelerated.

Strategy’s small BTC sale weakened the “never sell” narrative and hurt market confidence.

Strong jobs data reduced Fed cut hopes, pushing yields higher and risk assets lower.

AI capital rotation, geopolitical risk, weak market structure, and early fear justified holding cash.

On Monday, June 2, Triton Liquid began exiting the market, and had sold 100% of our liquid assets by June 3.

Crypto Market Cap: Exit Zone & Re-Entry Levels

Please feel free to reach out to Charles if you'd like to schedule a market call with Triton.

Despite our enthusiasm around the fundamental growth this asset class has seen the past two years, we believe things will get worse before they get better. This note explains our reasoning.

To be clear - we are not sellers on deteriorating fundamentals - the projects we held during Q1 continue to generate real revenue and on-chain activity. We are sellers on risk-reward.

When the balance of evidence tilts decisively toward macro-driven downside, preserving capital is the strategy and Tuesday crossed that threshold.

What we were watching as of 5:00 PM ET, June 2

Price action: the break was decisive

BTC closed the day at ~$66,600, down 6.6% in a single session after failing to hold $71,000 support that had contained multiple prior tests.

ETH printed $1,856, a -7.4% daily decline, now -12% on the week.

SOL closed at $74, down 8.7% on the day - its lowest close in months.

ETF outflows: institutional hands folding

Bitcoin ETFs recorded 13 consecutive days of net outflows, totalling over $4.3 billion.

This is not retail panic but institutional de-risking at scale.

The last comparable streak preceded multi-week drawdowns in both duration and magnitude.

Strategy: the "never sell" narrative breaks

On June 1, Strategy (formerly MicroStrategy) disclosed in an SEC filing that it had sold 32 BTC — its first Bitcoin sale in nearly four years — to fund preferred dividend obligations.

Michael Saylor, who built his entire brand on "never sell," framed it as routine treasury management.

When the most convicted institutional Bitcoin holder on the planet becomes a seller, it removes a psychological floor. The signal was not the size but what it implied about the conditions that forced the decision.

Strategy's stock dropped nearly 6% on the news. MSTR had functioned as a leveraged proxy for institutional Bitcoin conviction; its breakdown was a leading indicator, not a lagging one.

The fear here is less around long-term BTC implications, but more centered in the perception of Saylor as a potential seller will scare people away from the asset, near-term.

Macro: the rate cut thesis is off the table, for now

May non-farm payrolls came in well above consensus, erasing any residual probability of a near-term Fed rate cut.

10-year Treasury yields rose in response; risk assets across equities, commodities, and crypto sold off in tandem.

Our regression models consistently show macro as the dominant explanatory variable across our 27 verticals. When that variable turns, everything else becomes noise.

AI & IPO pipeline: the marginal dollar has a better offer

While crypto sold off, global equities hit fresh all-time highs - the Nasdaq and S&P 500 continued setting records as AI-related stocks absorbed the capital that was leaving digital assets.

K33 Research noted on June 2: "Much of the market views the opportunity cost of holding BTC as too high while anything AI-related soars."

SpaceX was targeting a Nasdaq listing on June 12 at a valuation of ~$1.75 trillion; OpenAI was targeting a public listing as early as September; Anthropic submitted its S-1 on June 1 at a $965 billion valuation. Taken together, the three candidates represent a valuation block of well over $4 trillion - all competing for the same institutional capital.

Crypto's $250B decline while stocks remained near record highs supports the capital-rotation theory.

Middle East: geopolitical premium re-entering

U.S.-Iran exchanges escalated materially in the days preceding the sell-off.

Energy and commodities dislocations were already repricing global risk; crypto, as the highest-beta risk asset, was last in line to reflect it - and then did so sharply.

Market structure: no floor visible

Bitcoin dominance remained elevated (~56%), meaning alts were absorbing disproportionate selling pressure.

Crypto-linked equities (MSTR, COIN, MARA) had already been breaking down for days - a leading indicator that went unheeded by spot.

No visible institutional bid; order book depth had thinned materially.

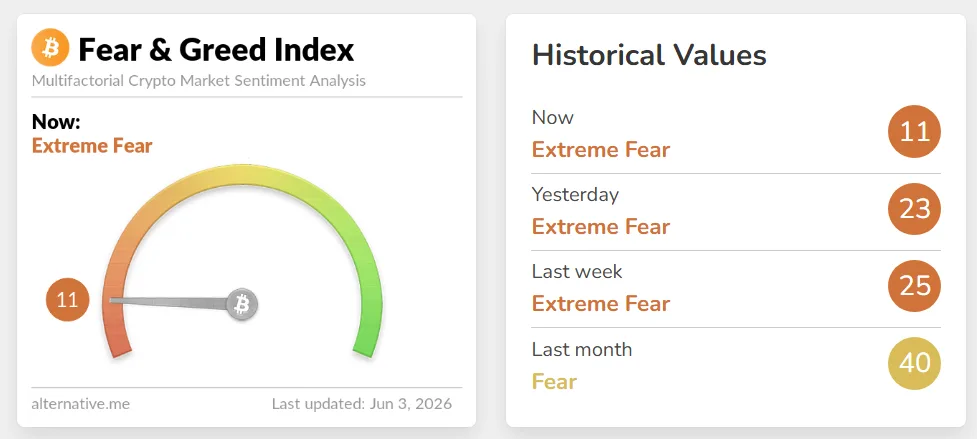

Sentiment: not the kind of fear that creates opportunity

The Crypto Fear & Greed Index was deep in fear territory, but the character of this fear was different: it was not the capitulation-driven fear that marks bottoms; it was the early-stage fear that precedes further selling as more participants reassess exposure.

There is a version of fear that is an entry signal - when on-chain metrics, long-term holder behaviour, and exchange flows confirm exhaustion. We described exactly that in Q1 2026 (MVRV at 1.35, exchange balances -30K BTC, realized losses at $2.1B). That is not what June 2 looked like. It looked like a market that had not yet found its clearing price, with macro headwinds still building and institutional flows still pointing outward.

We hold cash. We are watching. The next piece will outline what we need to see before we get back in.

On rare occasions, we publish our highest-conviction investments. This week, Triton initiated a position in Hypercall (SYN). Our view: the market is pricing its past, while overlooking Hypercall's potential as a leading on-chain options platform.

Triton fully exited liquid assets by June 3 as macro pressure, ETF outflows, weak market structure, and capital rotation turned crypto risk-reward negative. The decision was not driven by broken fundamentals, but by a market where downside risk outweighed upside until clearer re-entry signals emerge.

We see Q1 2026 as a rare asymmetric crypto entry point—fundamentals are intact, valuations reset, and sentiment is at multi-year lows—positioning our long-horizon capital to capture potential outsized returns through our vertical-focused, data-driven approach.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Triton Limited is incorporated in the Abu Dhabi Global Market (“ADGM”) and is regulated by the Financial Services Regulatory Authority (“FSRA”) under Financial Services Permission number 240017.