Disclaimer: For Professional Clients only. This document is provided for information purposes only and does not constitute investment advice, an offer, or a solicitation to invest in any financial instrument or fund. The views expressed are subject to change and should not be relied upon for investment decisions. Certain statements may include forward-looking views which are subject to risks and uncertainties. Triton may maintain positions in the assets or protocols discussed. References to protocols, venues, or tokens are for illustrative purposes only and do not constitute recommendations or indications of current or future portfolio positioning. Triton Limited is incorporated in the Abu Dhabi Global Market (“ADGM”) and is authorised and regulated by the Financial Services Regulatory Authority (“FSRA”) under Financial Services Permission number 240017.

TL;DR

Perpetuals Have Already Won the First Market

Perpetual swaps did not catch on because they were novel, but because they solved a practical problem better than the available alternatives. Traders wanted continuous leverage exposure without rolling fixed expiries, and crypto was the first market where that structure could scale cleanly.

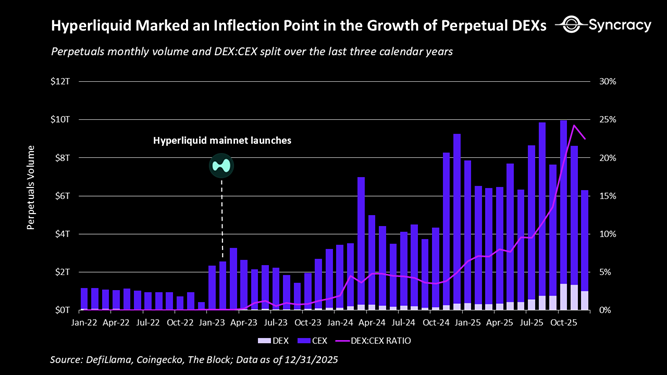

The adoption data increasingly supports that conclusion. CoinGecko estimates that the top 10 perpetual DEXs traded $6.7 trillion in 2025, up from $1.5 trillion in 2024. Over the same period, the perp DEX:CEX volume ratio rose from 2.5% to 7.8%. The market remains centralized in absolute terms, but decentralized share is no longer negligible.

The Q4 step-up was especially notable. Top-10 perpetual DEX volume rose 80.8% quarter-on-quarter, from $1.8 trillion in Q3 to $3.2 trillion in Q4. That does not mean the category has already matured, but that perpetuals are no longer a crypto-native curiosity.

Hyperliquid and the End of the Execution Objection

For several years, the standard objection to perpetual DEXs was straightforward: the product may have been compelling, but the venues were not yet competitive. Latency was high, books were thin, and liquidation systems were too fragile to support serious flow. That argument is weaker today than it was even eighteen months ago.

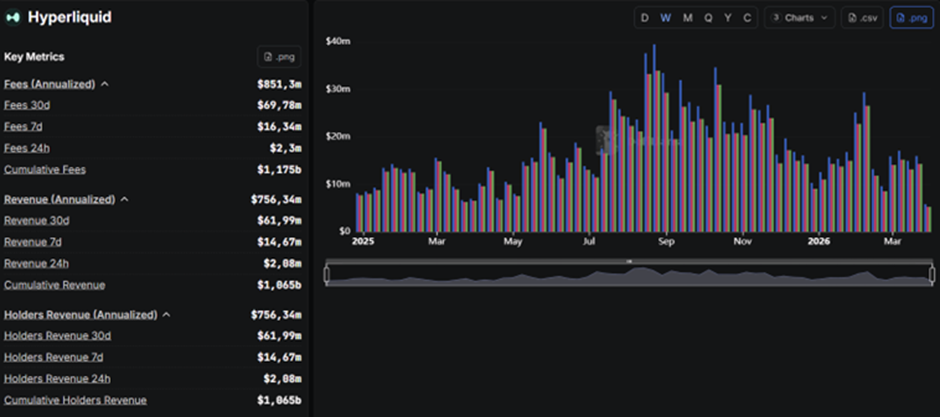

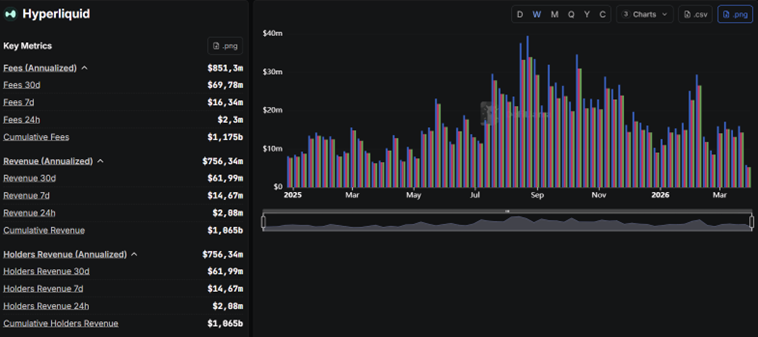

Hyperliquid is the clearest example. DefiLlama shows gross protocol revenue of $354.9 million in Q3 2025 and $286.5 million in Q4 2025, followed by $199.6 million in Q1 2026 to date. The revenue base remained heavily skewed toward perpetual trading fees. CoinGecko’s 2024 review also showed Hyperliquid accounting for more than half of top-10 perp DEX volume in Q4 and roughly two-thirds of open interest by year-end.

Decentralized execution quality is no longer easy to dismiss on first principles. At current scale, the more relevant question is whether perpetual DEXs can retain depth, liquidity, and risk discipline as market breadth expands.

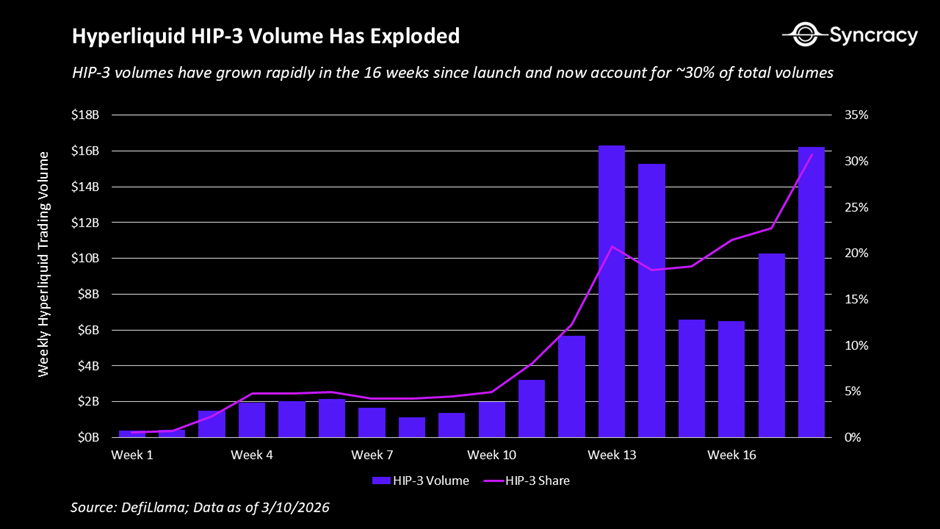

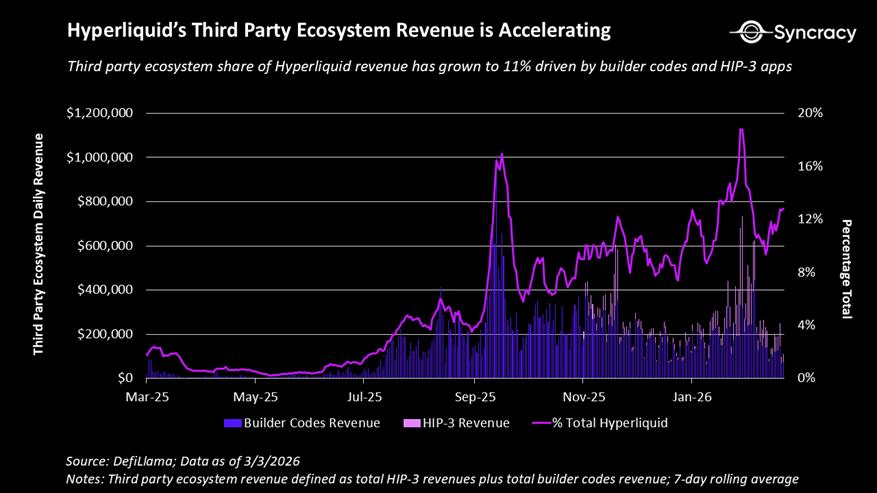

HIP-3 and the Expansion Beyond Crypto

The strategic importance of HIP-3 is that it moves Hyperliquid beyond a venue-led listing model and toward infrastructure-led market creation.

Under HIP-3, third-party deployers can launch perpetual markets on Hyperliquid’s order book subject to defined requirements, including a 500,000 HYPE stake for mainnet deployment. Hyperliquid’s documentation also makes clear that HIP-3 markets begin as isolated-margin products and that deployers participate directly in fee economics.

That change matters because perpetuals do not require full on-chain transfer of the underlying asset in the way spot tokenization does. They require collateral, market design, and a price feed that participants trust. In practice, that creates a faster path to on-chain exposure for equities, commodities, indices, and other non-crypto assets.

This is one reason the HIP-3 framework matters more than the headline around “everything exchanges.” It is not simply a slogan about asset breadth. It is a mechanism for expanding market coverage without rebuilding the core venue each time.

Where the Demand Is Most Likely to Come From

At this stage, one of the more credible expansion paths beyond crypto appears to be retail speculative flow rather than institutional hedging.

That demand is already visible in adjacent markets. Cboe reported 15.2 billion listed options contracts traded in the United States in 2025. Average daily volume remained concentrated in index, ETF, and single-stock products, while SPX 0DTE volume averaged 2.3 million contracts per day and accounted for 59% of total SPX options volume. The CFTC’s 2024 work on retail futures traders pointed to similarly short holding periods, with the median trader in its sample appearing for only a small number of trades held for a matter of days.

The pattern is fairly clear. A meaningful share of retail derivatives activity is not being used to express complex volatility views or manage long-dated physical exposures. It is being used to express short-horizon directional risk.

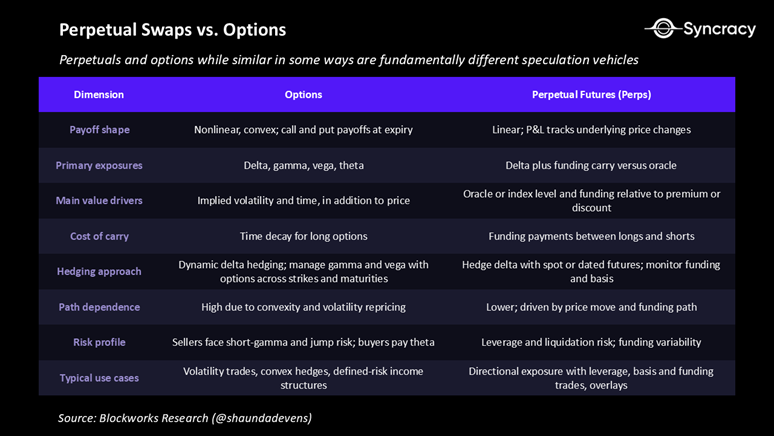

That is where perpetuals fit naturally. They offer linear exposure, no strike selection, no expiry roll, and no theta decay. That does not make them superior to options in every setting. It does suggest they are better aligned with a meaningful part of the use case now being served by short-dated listed options.

The Cleaner Substitution Case Is CFDs

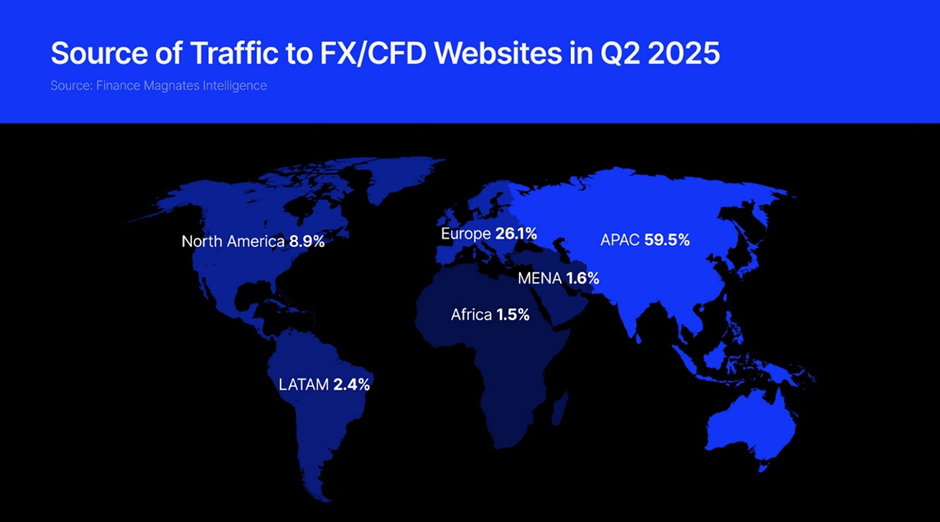

The comparison with CFDs is more direct. Finance Magnates reported that global retail FX and CFD trading volumes exceeded $30 trillion per month in Q2 2025, with traffic remaining heavily concentrated in Asia-Pacific.

Mechanically, CFDs already approximate much of the economic exposure that perpetuals provide: leveraged directional positioning without ownership of the underlying and, in many cases, without fixed expiry. The difference is structural. CFDs sit inside broker-specific bilateral agreements, with fragmented liquidity, discretionary spreads, and direct counterparty dependence on the broker. Perpetuals can deliver a similar use case through a visible order book with more standardized rules and more transparent risk transfer.

For that reason, the substitution case looks stronger against CFDs than against listed options. Options still retain clear utility in volatility trading, convex hedging, and defined-loss structures. CFDs are much closer to perpetuals in economic function, but generally weaker in market structure.

24/7 Access Matters, but It Is Not the Whole Thesis

The 24/7 argument is real, but it should be kept in proportion.

Traditional exchanges are already moving in this direction. Nasdaq said in late 2025 that it planned to extend trading on its U.S. equities venue toward 24-hour, five-day operation, subject to approval. Cboe has also expanded trading hours in major index options. That matters because it suggests demand for broader market access is already visible within legacy market structure.

What longer trading hours do not solve on their own is the deeper structural issue. Extending session length is not the same as replicating a unified perpetual stack with always-on collateral, continuous margining, and integrated liquidation logic. That remains a meaningful distinction between legacy venues and on-chain perpetual markets.

The Core Structural Advantage

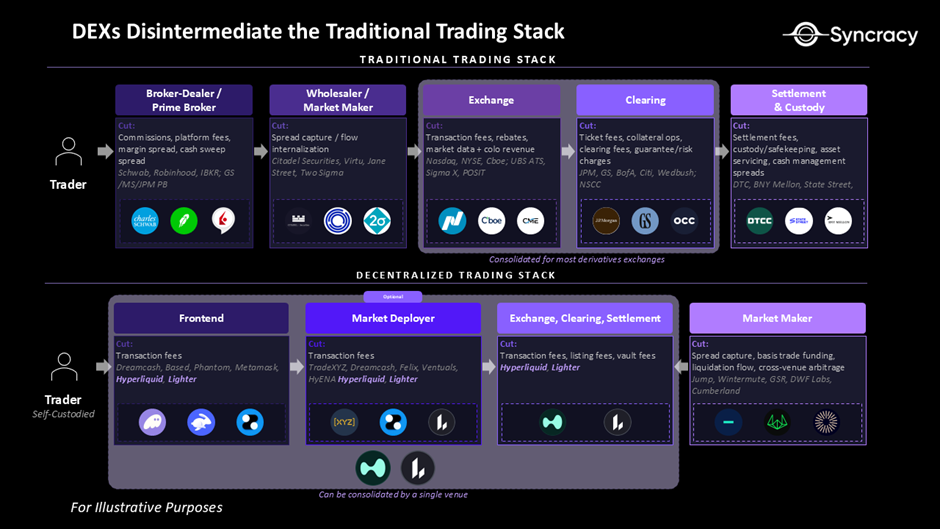

One of the strongest structural arguments for decentralized perpetual exchanges is not ideological. It is operational.

A perpetual DEX compresses more of the trading stack into one system. Market access, collateral management, liquidation logic, and settlement sit closer together than they do in the traditional model, where brokers, exchanges, and clearing entities remain functionally distinct.

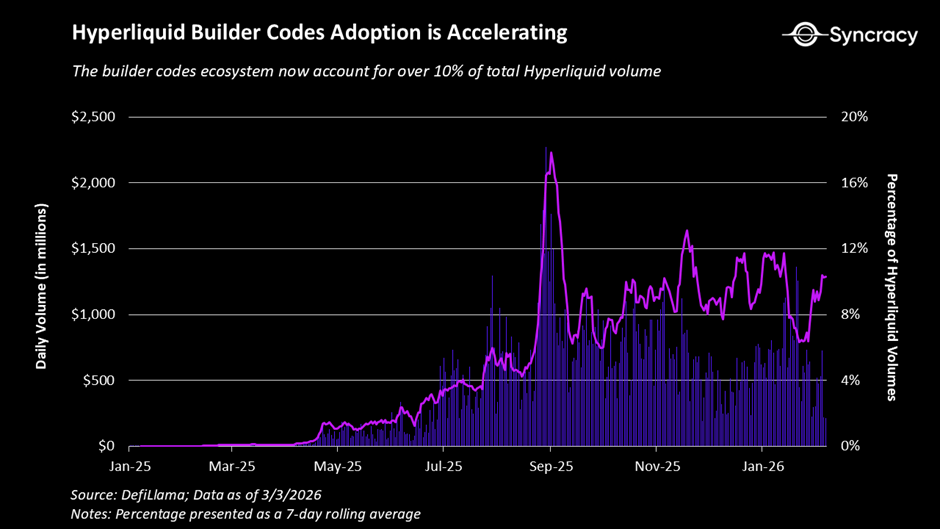

There is also a distribution advantage. Hyperliquid builder codes allow third parties to route flow and participate directly in fee economics. DefiLlama’s revenue presentation now explicitly breaks out builder-code-related fees from perp and spot fees, which makes the ecosystem layer observable rather than theoretical.

That architecture does not remove the difficult parts. It changes where the constraints sit. The open questions are now around non-crypto liquidity quality, stress behavior, market design for new assets, and regulatory treatment, rather than whether decentralized venues can host perpetuals at all.

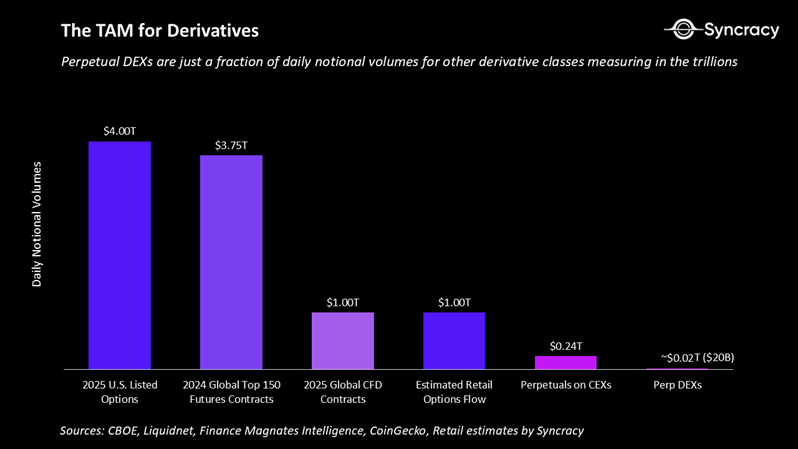

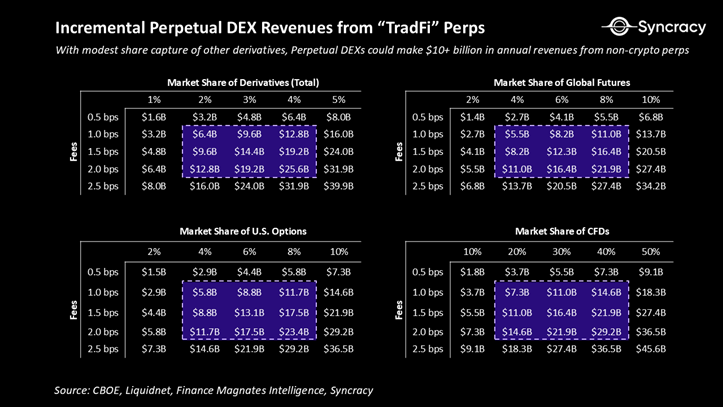

Market Size and What Is Actually Addressable

The global derivatives complex is large enough that the opportunity can easily be overstated.

A more useful framing is narrower. The relevant near-term pool is not the entirety of global derivatives turnover. It is the portion of retail and speculative flow currently expressed through short-dated options, CFDs, and part of listed futures activity.

Cboe’s 2025 options data and Finance Magnates’ CFD estimates make clear that those adjacent markets are already very large. Against that backdrop, CoinGecko’s estimate of $6.7 trillion in annual top-10 perp DEX volume is still small in relative terms.

That is the more credible underwriting case. Perpetual DEXs do not need to replace the global derivatives market to matter. They need to continue taking share within a narrower but high-turnover segment of speculative flow.

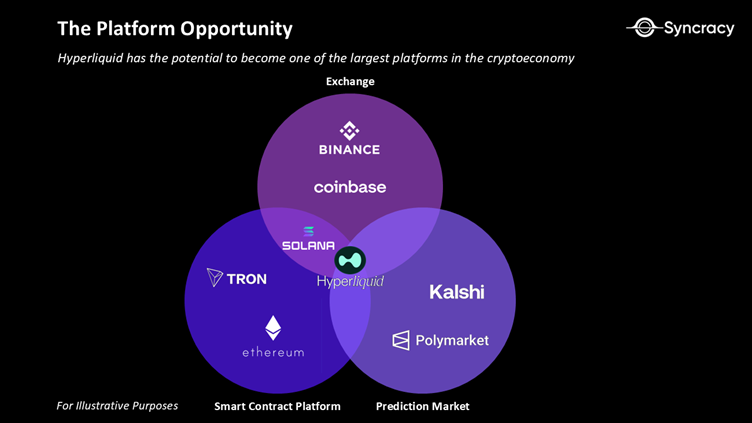

Optionality Beyond Perpetuals

There is a broader platform argument here, but it should remain second-order.

If a venue can support perpetual trading at scale with credible liquidations and consistent collateral logic, adjacent products become easier to add. Spot, options-like structures, vaults, prediction markets, and cross-product margining all become more plausible extensions.

That may matter a great deal over time. It is not, however, the first thing that needs to be underwritten. The base case still rests on whether perpetual DEXs can retain non-crypto flow, maintain execution quality, and continue compounding liquidity.

Valuation and Revenue Sensitivity

The revenue opportunity does not require aggressive assumptions to become meaningful. Even modest share capture within adjacent retail derivatives markets would expand the addressable revenue base materially, particularly given the fee profile and operating leverage already visible in leading venues.

That still needs to be framed with care. The relevant opportunity is not the entirety of global derivatives turnover, but a narrower slice of retail and speculative flow where perpetuals are structurally competitive. Even under that narrower framing, low single-digit share capture can support a substantially larger revenue base than the market appears to be discounting today.

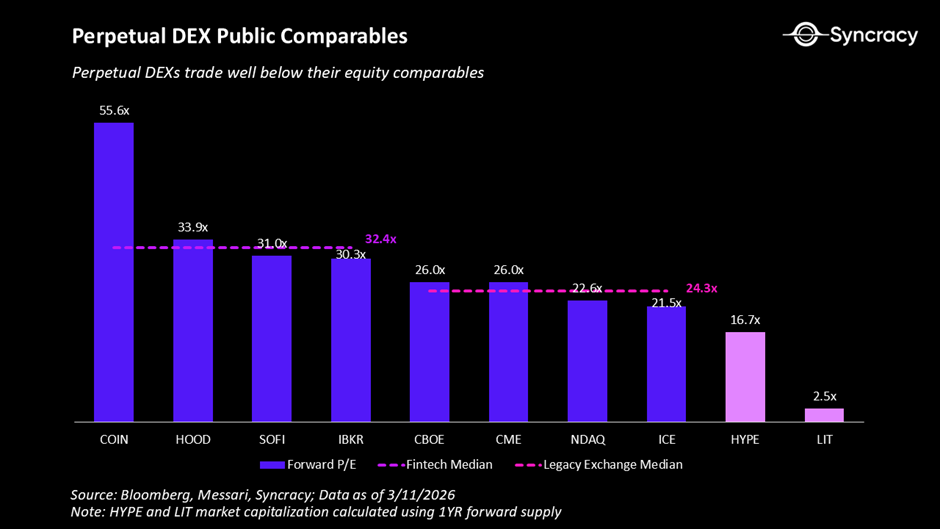

Current market pricing remains relatively restrained against that backdrop. On Syncracy’s estimates, leading perpetual DEX tokens continue to trade below a range of fintech and exchange comparables, which current valuations appear more aligned with a scenario in which decentralized venues capture even a modest share of adjacent non-crypto flow.

A more constructive long-term outcome would require several things to go right at once: continued liquidity growth, acceptable execution quality in non-crypto markets, stable risk management through stress, and a regulatory backdrop that does not materially impair venue expansion. Those conditions are not yet secured, but neither are they reflected in current pricing.

Taken together, the valuation case is not that perpetual DEXs need to displace the incumbent market structure outright. It is that current market pricing still appears to assume a relatively narrow end state for a category that has already demonstrated product-market fit in crypto and is beginning to test adjacent markets under live conditions.

Conclusion

The core thesis is straightforward. Perpetuals have already established product-market fit in crypto, and Hyperliquid shows that a decentralized venue can now operate at meaningful scale. The more credible path beyond crypto is not wholesale replacement of incumbent market structure, but gradual share capture in retail and speculative flow, where short-horizon leveraged exposure is the dominant use case.

We touched on part of this dynamic in our earlier note, The Best Business(es) in the World?, which examined the unusually lean economics of crypto-native platforms at scale. Hyperliquid featured prominently there as an early example of how an on-chain exchange can turn volume, fee capture, and market structure into a business model that may, in certain contexts, compare competitively with traditional venues.

What matters from here is execution. The next phase of the category will be determined by a short list of observable metrics: retention in non-crypto markets, liquidity quality outside core crypto pairs, funding stability, liquidation performance through stress, builder ecosystem growth, and regulatory response. If those improve, the structural case strengthens. If they do not, perpetual DEXs remain important inside crypto, but narrower outside it.

Digital assets are highly volatile and may result in partial or total loss of capital. Past performance and market indicators are not reliable indicators of future results. Investors should conduct their own independent assessment before making any investment decision.

On rare occasions, we publish our highest-conviction investments. This week, Triton initiated a position in Hypercall (SYN). Our view: the market is pricing its past, while overlooking Hypercall's potential as a leading on-chain options platform.

Triton fully exited liquid assets by June 3 as macro pressure, ETF outflows, weak market structure, and capital rotation turned crypto risk-reward negative. The decision was not driven by broken fundamentals, but by a market where downside risk outweighed upside until clearer re-entry signals emerge.

We see Q1 2026 as a rare asymmetric crypto entry point—fundamentals are intact, valuations reset, and sentiment is at multi-year lows—positioning our long-horizon capital to capture potential outsized returns through our vertical-focused, data-driven approach.