Disclaimer: For Professional Clients only. This document is provided for information purposes only and does not constitute investment advice, an offer, or a solicitation to invest in any financial instrument or fund. The views expressed are subject to change and should not be relied upon for investment decisions. Certain statements may include forward-looking views which are subject to risks and uncertainties. Triton may maintain positions in the assets or protocols discussed. Triton Limited is incorporated in the Abu Dhabi Global Market (“ADGM”) and is authorised and regulated by the Financial Services Regulatory Authority (“FSRA”) under Financial Services Permission number 240017.

TL;DR

With the broader market still trading through the aftermath of deleveraging, the next question is where structural activity remains strongest beneath the surface. The assets and protocols below are not grouped on the basis of short-term price performance, but rather by the durability of their underlying activity, market position, and ability to retain relevance through a weaker tape.

What follows is a set of focused asset notes across several of the ecosystems and protocols we continue to monitor, including Solana, Maple, Hyperliquid, Pendle, and Aerodrome. In each case, the goal is not to force a bullish conclusion, but to assess whether current usage, capital flows, and protocol mechanics may support a constructive medium-term view despite continued macro uncertainty.

Asset Notes

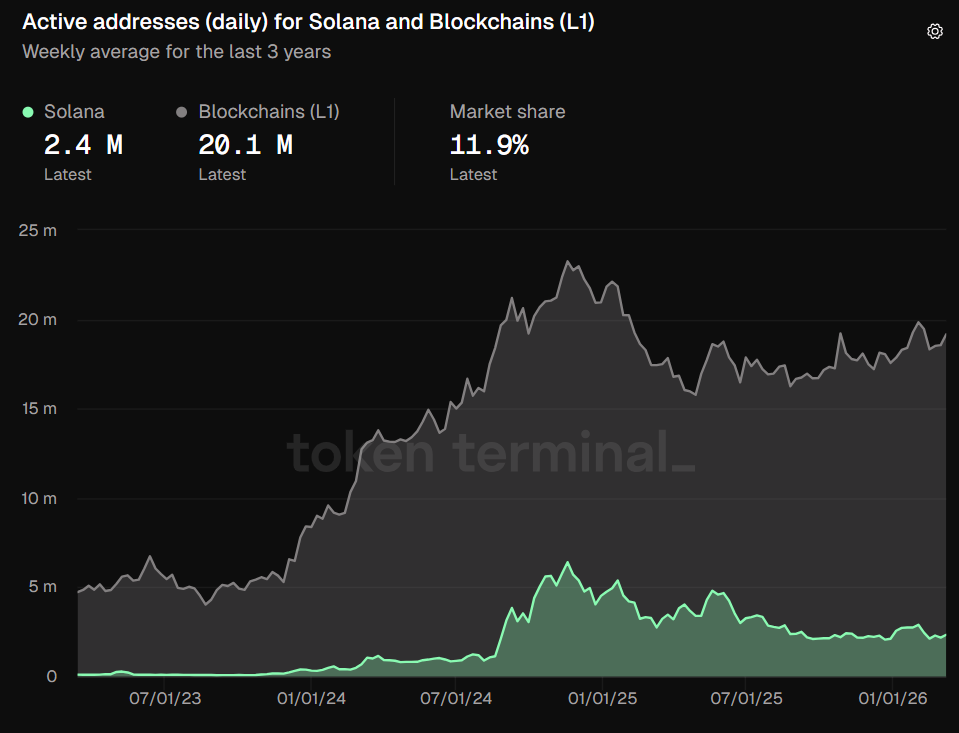

Solana (SOL)

Solana network activity has stabilized following the sharp contraction from its late-2024 and early-2025 peaks. Weekly average active addresses recently stood at approximately 2.4 million, representing roughly 11.9% of tracked Layer 1 activity. This marks a recovery from the weaker levels seen in late 2025, though activity remains well below the highs reached during the prior expansion phase.

Activity previously reached materially higher levels during the 2025 expansion before cooling alongside broader market deleveraging. Looking ahead, Solana’s 2026 technical roadmap includes Firedancer, a second validator client progressing toward mainnet readiness, which is expected to improve validator diversity and expand network throughput capacity as activity scales.

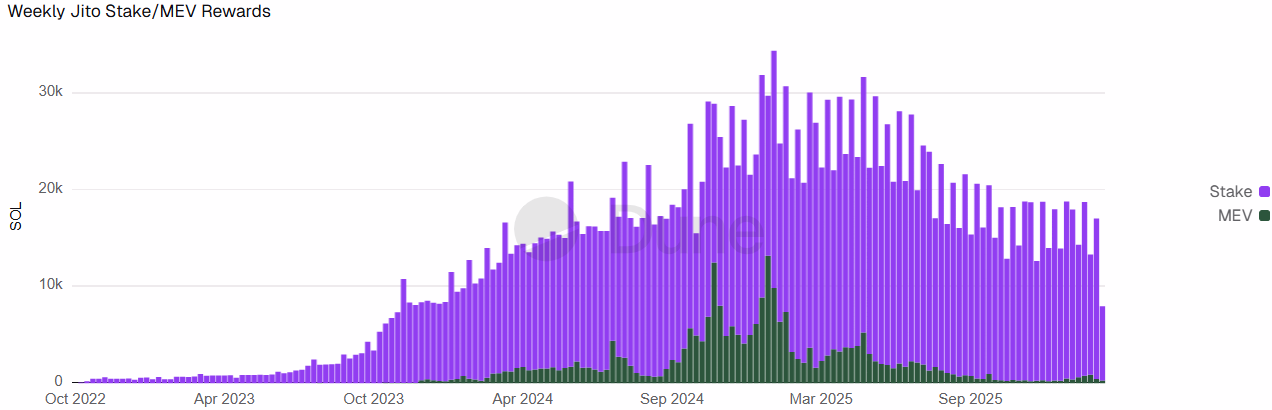

Weekly staking rewards have moved with the broader cycle, but within a noticeably tighter range than spot prices. The staking component built steadily through 2023 and 2024, peaked during the high-activity window, and then compressed into late 2025, while the MEV component has been more episodic, spiking during periods of elevated transaction competition and fading as activity and priority-fee intensity normalized. The net effect is that total rewards remain positive, but the incremental MEV uplift has been smaller than during the prior peak period, consistent with a cooler tape.

Maple Finance (SYRUP)

Maple remains a meaningful venue within tokenized private credit. On RWA.xyz, Maple shows $1.864 billion in active loans against $8.332 billion in total historical loan volume, with an average base APY of 9.01% and $47.1 million listed as defaulted loan amount. DeFiLlama reports $1.859 billion of TVL and $1.836 billion borrowed. The proximity of TVL and borrowed, with borrowed capital at approximately 99% of TVL, is consistent with capital being deployed rather than sitting idle.

In context, RWA.xyz reports $22.20 billion in active loans value across tracked tokenized private credit platforms, with $40.11 billion in total historical loans value. Maple’s $1.864 billion in active loans implies roughly 8.4% of active outstanding value on that dataset, placing it among the larger venues by outstanding loan value. The broader takeaway is narrow but important: tokenized private credit has scaled into a measurable on-chain vertical with multiple platforms operating at multi-billion-dollar outstanding balances, even as crypto spot markets have remained volatile.

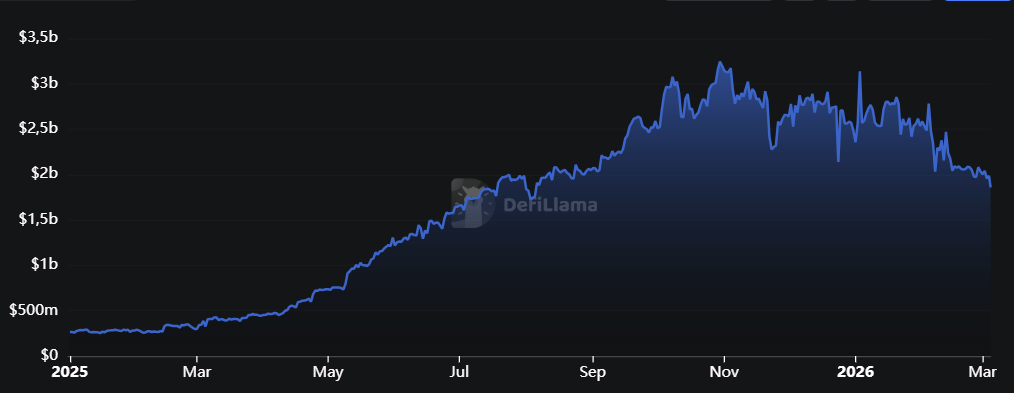

Hyperliquid (HYPE)

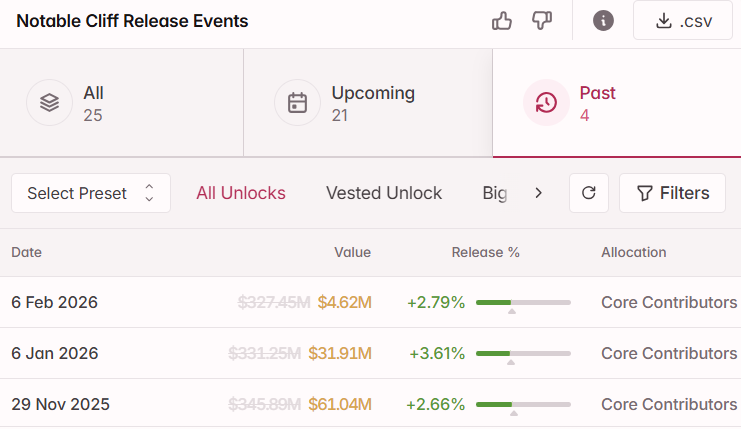

Hyperliquid remains one of the most important venues in on-chain derivatives. As of early March 2026, open interest stood at approximately $5.8 billion, keeping the platform in the mid-single-digit billion range even after a material pullback from the highs reached in 2025. Separately, the core contributor allocation, representing roughly 23.8% of total HYPE supply, began vesting in January 2026, with approximately 1.2 million tokens released monthly.

The late-February 2026 weekend provided a useful illustration of the structural characteristic of continuous markets. During a period of material geopolitical escalation, traditional commodity venues were closed, while commodity-linked perpetuals on Hyperliquid continued trading. That is not a promotional claim; it is a market-structure observation. On-chain derivatives venues remained open and provided price discovery while much of traditional finance was offline.

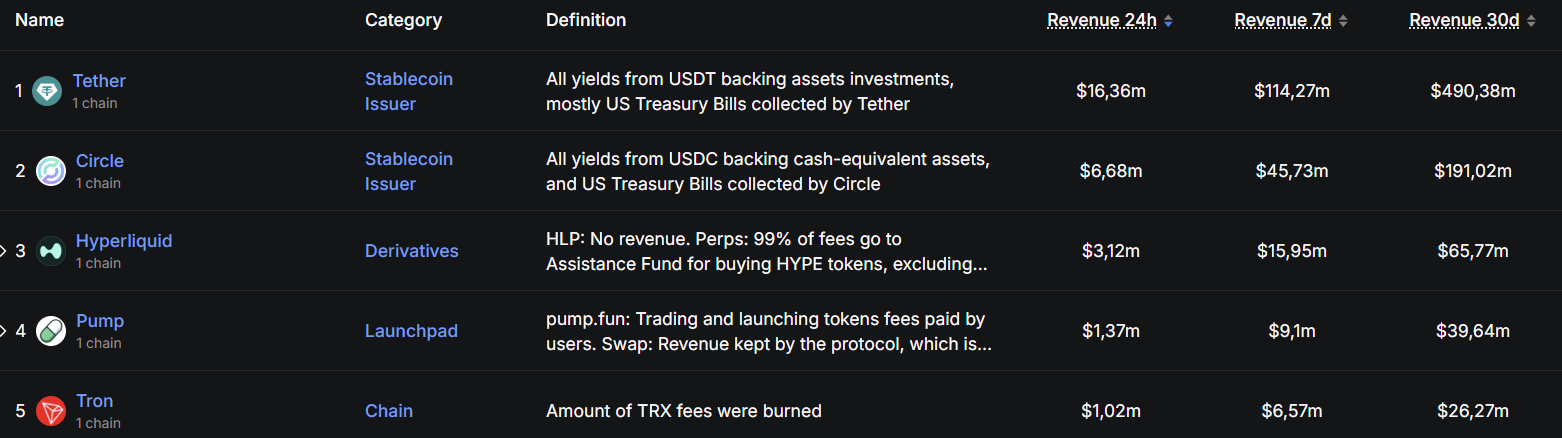

The mechanism is what matters. Always-on markets with transparent on-chain settlement may provide certain operational benefits during periods of elevated event risk. Participants with access to continuous commodity-linked perpetuals can hedge or express macro views in real time, while those constrained to traditional market hours face execution gaps when markets are closed. Hyperliquid’s continued position among the top revenue-generating on-chain venues reinforces the point that derivatives activity remains structurally important even in a weaker tape.

Pendle (PENDLE)

In January 2026, Pendle replaced its vePENDLE two-year lock mechanism with sPENDLE, a liquid staking model featuring a 14-day withdrawal period. The protocol now directs revenue toward PENDLE buybacks rather than emissions-based rewards, aiming to create a more direct value-accrual mechanism while simplifying the user experience. Weekly governance votes have also been eliminated, reducing operational friction for token holders.

The upgrade is designed to improve accessibility for capital previously constrained by long-dated lockups. Pendle has indicated a target staking rate of 15-20% under the new structure and estimated to have roughly 30% lower liquidity incentive requirements due to improved capital efficiency. DeFi composability has been preserved, creating clearer pathways for integration with lending protocols such as Aave. Existing vePENDLE holders also received transition reward boosts during the migration period.

As of March 5, 2026, Pendle maintained approximately $2.21 billion in TVL across Ethereum ($1.02 billion), Plasma ($850 million), and Arbitrum ($214 million). The protocol has also expanded into real-world asset markets, with $376.5 million in RWA TVL and $56.5 million deployed as RWA-backed collateral on Morpho, representing approximately 17% of all RWA collateral on that platform.

Aerodrome (AERO)

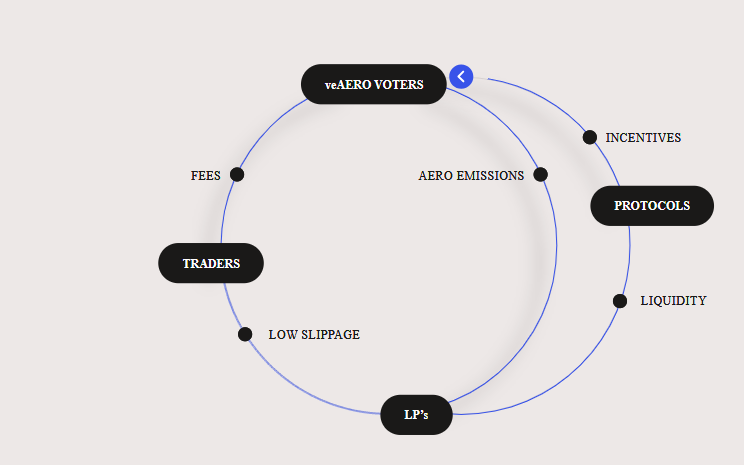

Aerodrome remains the dominant decentralized exchange on Base, consistently accounting for a majority share of network DEX activity. The protocol’s model is unusual in that 100% of trading fees are distributed to veAERO voters, rather than being retained by a treasury, creating a direct linkage between trading activity and governance participation.

The protocol exhibits relatively high beta to broader crypto risk appetite, meaning performance has historically been highly sensitive to shifts in market sentiment and Base ecosystem activity. That sensitivity cuts both ways: Aerodrome has tended to outperform during stronger recovery phases, but it has also retraced materially during broader risk-off periods. For that reason, the cleaner takeaway is not directional optimism but operating leverage to improving conditions on Base.

In November 2025, Aerodrome announced a broader expansion strategy through a unified platform called Aero, designed to connect Aerodrome on Base with Velodrome on Optimism while expanding to Ethereum mainnet and Circle’s Arc blockchain. The stated goal is to broaden liquidity access beyond Base and position the protocol as a wider cross-chain liquidity hub rather than a single-network exchange.

Conclusion

Across these asset notes, the common thread is not immunity to market weakness, but continued relevance despite it. Activity has cooled in some areas and beta remains high across much of the sector, yet the protocols discussed here still show measurable signs of structural durability, whether through sustained usage, growing TVL, persistent market share, or improved value-accrual mechanisms.

Solana continues to retain meaningful network activity while advancing technical upgrades that could matter more in the next expansion phase than in the current one. Maple remains positioned within one of the clearest real-world adoption verticals in crypto, with tokenized private credit still scaling even through volatile market conditions. Hyperliquid continues to demonstrate the importance of always-on derivatives infrastructure, particularly during periods of heightened macro stress. Pendle’s redesign simplifies participation while reinforcing value capture, and Aerodrome remains a high-beta expression of Base ecosystem activity with direct exposure to improving on-chain trading conditions.

Taken together, these are not asset-specific arguments for immediate upside. They are observations about where fundamentals still appear intact, where protocol design continues to evolve constructively, and where activity has remained resilient enough to justify continued attention. In a market still defined by macro uncertainty and cautious re-risking, that distinction matters.

Digital assets are highly volatile and may result in partial or total loss of capital. Past performance and market indicators are not reliable indicators of future results. Investors should conduct their own independent assessment before making any investment decision.

On rare occasions, we publish our highest-conviction investments. This week, Triton initiated a position in Hypercall (SYN). Our view: the market is pricing its past, while overlooking Hypercall's potential as a leading on-chain options platform.

Triton fully exited liquid assets by June 3 as macro pressure, ETF outflows, weak market structure, and capital rotation turned crypto risk-reward negative. The decision was not driven by broken fundamentals, but by a market where downside risk outweighed upside until clearer re-entry signals emerge.

We see Q1 2026 as a rare asymmetric crypto entry point—fundamentals are intact, valuations reset, and sentiment is at multi-year lows—positioning our long-horizon capital to capture potential outsized returns through our vertical-focused, data-driven approach.