Disclaimer: This is not financial advice. Anything stated in this article is for informational purposes only and should not be relied upon as a basis for investment decisions. Triton may maintain positions in any of the assets or projects discussed on this website.

TL;DR

Creativity in the Kitchen

Our past few posts have focused on the efficiency, size and profitability that well-designed blockchain protocols are able to achieve. Remarkably, growth seems to be accelerating. Aave – the decentralized lending protocol – has already added another $4.5 billion in deposits since our post in late August and is now just shy of $75B total. Meanwhile, Hyperliquid – the $120M profit-per-employee perpetual futures exchange that is already giving Nasdaq a run for its money – found itself in the middle of a bidding war over a single stablecoin ticker USDH, with some of the top protocols and companies in the industry, including the 400m user/trillion-dollar volume payments company Paypal, all fighting over the right to buy the ticker and be the ‘chosen’ stablecoin for Hyperliquid. Since we highlighted the exchange two weeks ago, HYPE has risen 28%, adding another $3.5 billion to its circulating market cap. Needless to say, the industry is pretty ~hyped about HYPE:

This week we will shift gears a bit and turn our attention to a small cap project building infrastructure on Solana. Specifically, we want to highlight how token-based businesses have an incredible design space to add additional value for token holders, a uniquely powerful tool when used in combination with the efficiency with which these projects can operate. We have frequently mentioned ‘tokenomics’ (e.g. the design of a token’s structure, utility and value capture) in the past but have never really explored how that can impact a protocol’s value. So, to do just that, we will provide a case study examining how one protocol completely revamped their tokenomic structure to dramatically improve the value of the protocol for potential investors, contributing to a rapid ~140% price appreciation over the course of just a few months.

Not Your Grandfather’s Marinade

Marinade is a decentralized staking protocol on Solana, providing infrastructure that enables investors in the SOL token to earn 7-10%+ yield on their holdings. Staking refers to the process of users depositing their tokens with network validators in order to help secure the network. In return, they earn a yield paid out from new network issuance (inflation), transaction fees paid by users of the chain, and validator priority fees earned for priority transaction inclusion (and their take from MEV). Typically, when one stakes SOL tokens with validators, those tokens become illiquid for as long as they are staked and there is a ~2 day ‘unbonding’ period to withdraw stake from validators (this varies by chain). For those looking for simple yield with a long-term view, this illiquidity is okay. But because of the opportunities within DeFi there is substantial opportunity cost associated with ‘native’ staking. So-called ‘liquid’ staking protocols have arisen to solve this issue. In short, liquid staking tokens (LSTs) allow for users to earn that yield while ALSO maintaining full liquidity on the token to send to others, to use as collateral in DeFi, or however they wish. That is, users deposit their SOL tokens into liquid staking contracts and receive a form of ‘receipt’ token that they can freely transfer or use.

This is the infrastructure that Marinade provides. The protocol primarily offers two products: its liquid staking token, mSOL, that allows users to hold a freely transferrable yield-bearing version of SOL, and a permissionless native staking protocol that offers instant unbonding for native stakers (e.g. staked tokens placed directly with validators), improving on the usual 2-day delay typically faced. To maximize rewards for their stakers, Marinade implements a unique auction mechanism where network validators bid to have Marinade stakers’ deposits directed to them, known as the ‘Stake Auction Marketplace’. This adds a third form of yield that Marinade is able to generate and distribute to its stakers.

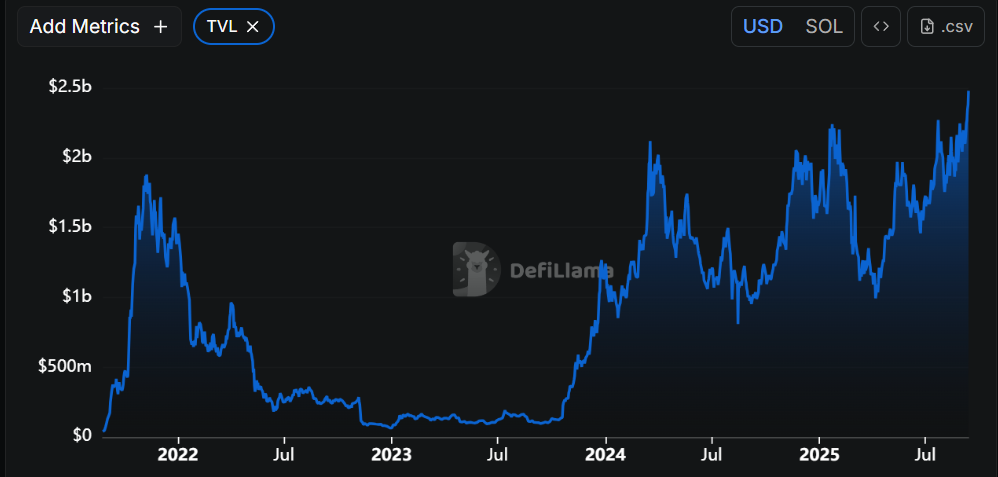

As of writing, Marinade has roughly $2.5B deposited in its protocol (referred to as ‘total value locked’ or TVL), and through its services generates nearly $170M per year in staking yield for its depositors. This size puts Marinade as a top-7 protocol on Solana in terms of TVL, and top-30 overall across the entire industry.

The Chefs Have Been Cooking

Despite this size and prominence, Marinade has historically not captured much value for token (MNDE) investors. The DAO realized this disconnect and embarked on a series of changes over the course of 2025 to strengthen the value of the protocol token. This provides us with an excellent case study to see in concrete terms how the fundamental value of the project was impacted by the tokenomic design, something normal equity investors do not regularly have to keep in mind (aside from normal capital structure considerations).

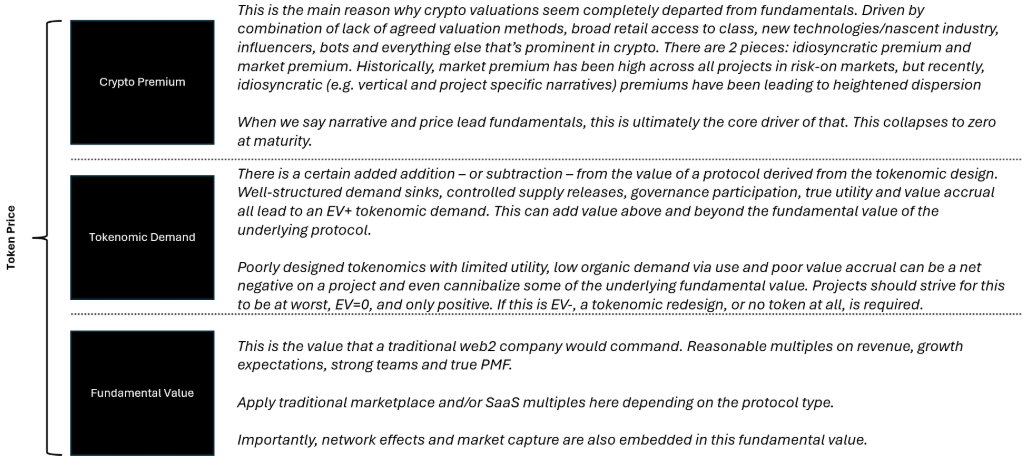

Long term readers of our posts may remember a simple three-part framework we use to understand value for tokens that includes: i) fundamental value, ii) crypto premium, and iii) tokenomic demand. We’ll use that as our starting point:

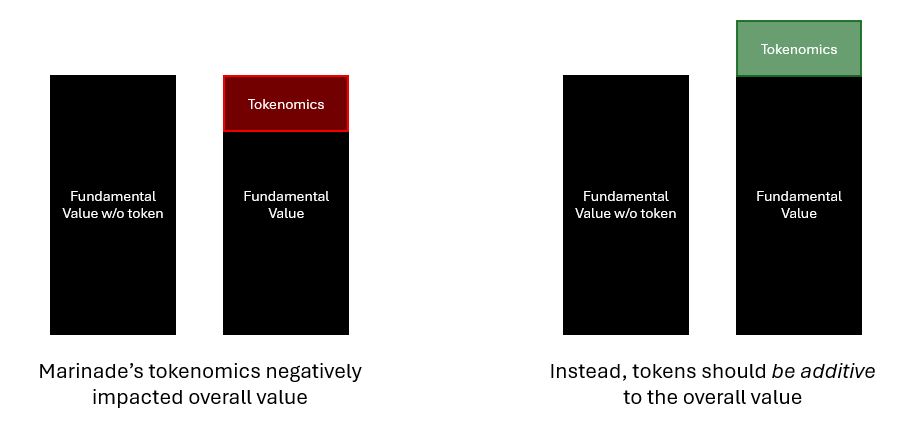

The fundamental value for Marinade was very solid - $2.5B in deposits makes Marinade one of the largest protocols in the entire industry - and the mSOL token has deep integrations across the Solana ecosystem. The project was also fair-launched and bootstrapped by a strong and growing team, there was no early investor supply overhang, and the DAO had control over protocol decisions and the $100M+ treasury. Despite this, the market cap of the project (even on a fully diluted basis) frequently traded barely above that treasury value. Why is that? It all comes down to the tokenomic structure. In short, the value capture of the token was so poor that it negatively impacted the overall value of the project. That dislocation was also an opportunity.

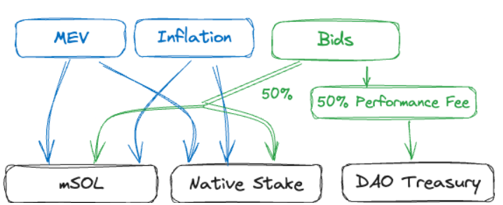

The initial model simply had all MEV/priority fees and inflation rewards directed to stakers, in addition to 50% of the marketplace bid (SAM) fees. The remaining 50% of the SAM fees went to the DAO treasury. This was generous for stakers but came at the expense of MNDE token holders; while MNDE holders theoretically had governance control over the treasury and thus the value that flowed there, that direct value accrual is not nearly as strong as token models with direct revenue shares or buybacks in place. Further, that SAM bid was relatively low compared to the size of MEV and inflation flows running through the protocol. As such, investors had to weigh this limited cash flow to the treasury (discounted further based on uncertainty around any timeline to actually realize that value) against any token incentive dilution and opportunity cost in the market. Too often, the value proposition came up short and the token price suffered as a result.

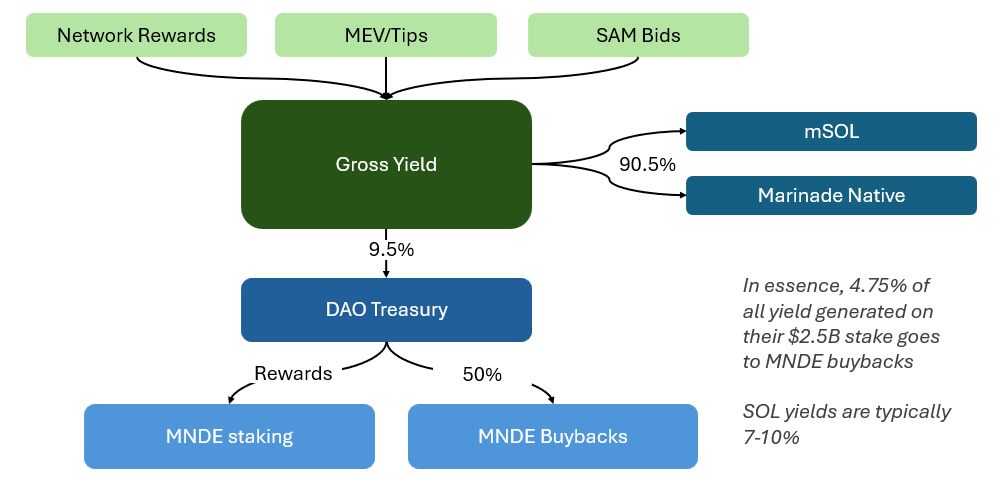

As a first step, the DAO approved a change (MIP-5) to strengthen flows to the treasury while at the same time implementing a new avenue through which MNDE holders could directly receive yield pass through from the revenue that the DAO earned. This new model included aggregating all yield sources into one gross pool from which 90.5% was passed through to stakers and 9.5% directed to the DAO. Of that 9.5%, 0.95% (i.e. 10% of the 9.5%) was available to holders of MNDE that chose to stake the token.

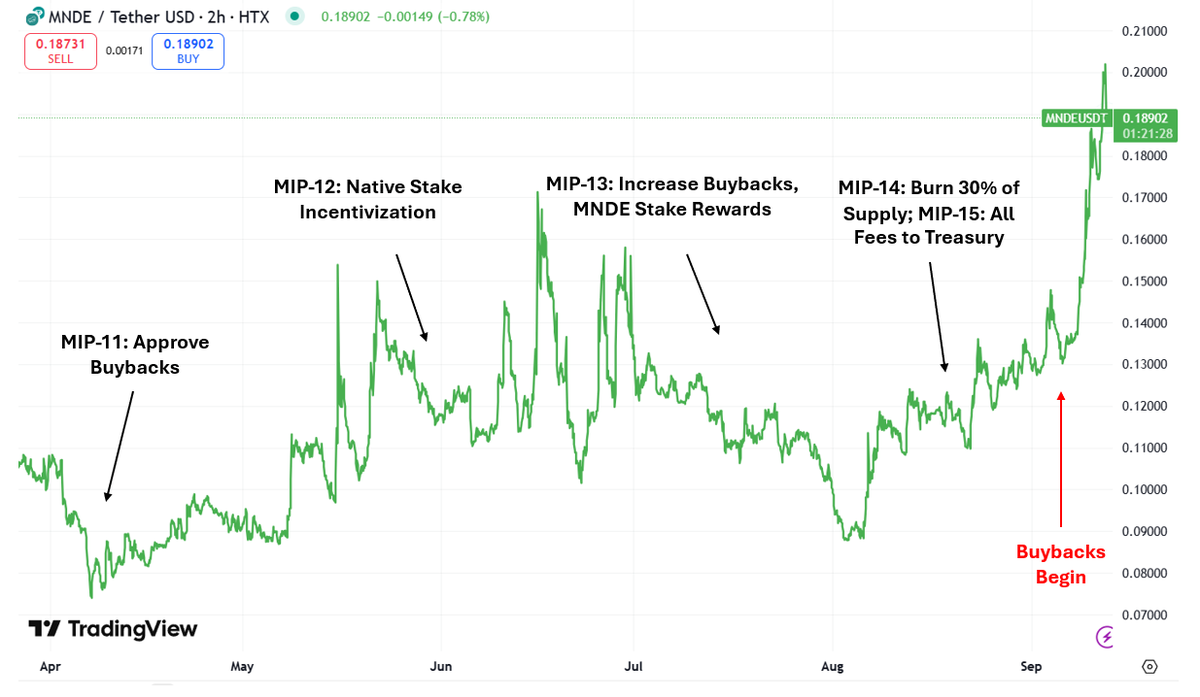

MIP-5 was a great first step, but 0.95% of ~7% yield on $2.5B is still pretty low – just ~$1.5-2M per year that gets passed through to token holders directly. To better bolster that value proposition, the DAO passed another proposal (MIP-11) that outlined the creation of a token buyback program. Simply, in addition to the 10% of treasury revenue that flows to MNDE stakers, another 40% would be directed towards buying back MNDE tokens on the open market and contributing them to the treasury. As is the case with traditional finance, token buybacks are similarly a tax-friendly method to share value with holders (vs. less tax friendly direct dividends). That resulted in another ~$6.5M annually of direct value accrual to the token. Most positively, these buybacks were to be implemented against a low float of circulating tokens – MNDE’s circulating market cap was well below $50M for much of 2025. $8M continued to flow to the protocol treasury.

This turned out to be an intermediate step as the MNDE staking mechanism did not see the desired uptake after going live. As such, the DAO passed a follow-on MIP-13 proposal that boosted the buybacks to a clean 50% of all DAO revenues and replaced the 10% that went to MNDE stakers with a rewards program sourced from MNDE’s treasury (~$2.5M worth of tokens). Importantly, only MNDE stakers that actively engage in DAO governance are now eligible to receive these rewards, further strengthening participation and rewarding participants that are long-term aligned. The tokenomic model now looks like this:

With this new structure, Marinade takes a cut of 9.5% of that ~$170M yield generated as revenue to the protocol, meaning it is earning ~$15-16M per year in revenue at current levels.

Of that, 50% goes directly to buying back the token off the open market. These repurchased tokens go to the Marinade treasury that the team can tap into to help incentivize growth, add onchain liquidity or help support its ecosystem in other ways, while token holders benefit from the continuous buy pressure hitting the charts.

As a final cherry on top, the DAO passed MIP-14 that resulted in burning (i.e. removing from circulation forever) 30% of the total supply of MNDE tokens, sourced from Treasury tokens. This is a very crypto-native use of funds and strong arguments can be made for and against whether this is the most effective way to utilize a balance sheet. Those in favor argue that by burning these tokens, that action reduces possible future dilution thus strengthening value accrual to tokens already in circulation. It is also largely seen as a positive signal to the market that the team has the interest of token holders at heart (surprisingly still not a given in the industry). On the flip side, 30% represents true value that the DAO held in treasury (30% of tokens was $40M at the time of the burn), and as such, served as a useful, monetizable capital asset. There are alternative uses that could arguably be more beneficial in the long run such as helping to grow the team, incentivizing mSOL or native-stake adoption, or providing additional liquidity for the market. Or, as a safety net, convertible to cash to fund operations if revenue slows.

Regardless, the market’s reaction to these changes, bolstered by continued asset growth alongside a rising SOL token price, proves many, if not all, of these changes are welcome. When MIP-11 (buybacks) was first being discussed, MNDE was trading at ~$0.075 (~$35M). Over the course of this tokenomic redesign, it has rebounded significantly and now trades at ~$0.19 ($90M) at the time of writing, a gain of roughly 140% in just a few months (some additional MNDE tokens have entered circulation, pushing up MC slightly relative to price). Some of this price performance is naturally from the market recovering from the April lows, but MNDE has been one of the strongest performing tokens in the market since that point.

Keep Sizzling?

One of the most innovative aspects of digital assets is that these instruments are live in terms of how they are structured and capture value. Teams can continuously improve upon tokenomic structure, tweaking it as necessity dictates in order to best maximize alignment with holders and ultimate value accrual. As new products are rolled out or as market conditions change (i.e. regulation), teams can (with the approval of DAO governance) fluidly adapt to the situation. Marinade’s tokenomic redesign over the past several months provides an excellent example of this mechanism in action and protocol stakeholders have been well rewarded as a result. It also allows us to provide more insight into how we as active token investors can take advantage of the major inefficiencies that still remain in the digital asset markets, contributing to our ability to generate venture-like returns while participating in 24/7 tradeable markets.

On rare occasions, we publish our highest-conviction investments. This week, Triton initiated a position in Hypercall (SYN). Our view: the market is pricing its past, while overlooking Hypercall's potential as a leading on-chain options platform.

Triton fully exited liquid assets by June 3 as macro pressure, ETF outflows, weak market structure, and capital rotation turned crypto risk-reward negative. The decision was not driven by broken fundamentals, but by a market where downside risk outweighed upside until clearer re-entry signals emerge.

We see Q1 2026 as a rare asymmetric crypto entry point—fundamentals are intact, valuations reset, and sentiment is at multi-year lows—positioning our long-horizon capital to capture potential outsized returns through our vertical-focused, data-driven approach.