Disclaimer: This is not financial advice. Anything stated in this article is for informational purposes only and should not be relied upon as a basis for investment decisions. Triton may maintain positions in any of the assets or projects discussed on this website.

TL;DR

“Aave Stadium” Coming To A Ballpark Near You?

With all of the newfound excitement around blockchain technology following the United States Government’s wide-armed embrace of the technology, we find many investors now asking us: “beyond the chains, what is investable?”. And aside from those who are deep into the weeds of the crypto market, most are pretty surprised to hear about the magnitude of some of these decentralized, onchain businesses. With that in mind, we will focus this post on one of the most prominent examples of product-market-fit for blockchain technology: decentralized money markets.

Bank Business Model: Match Depositors and Borrowers

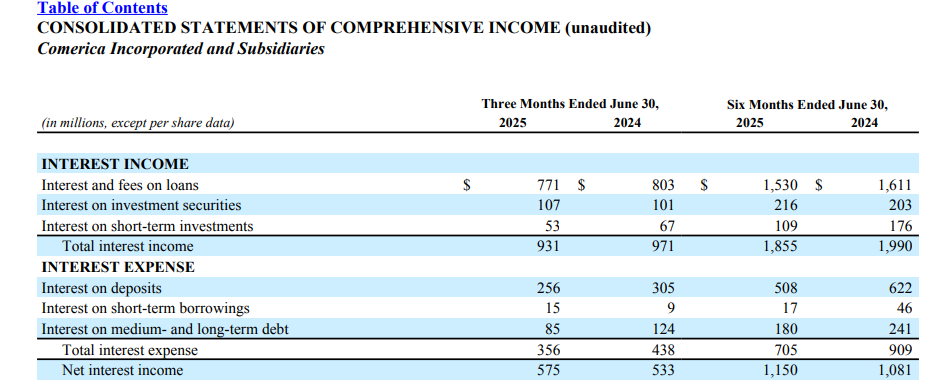

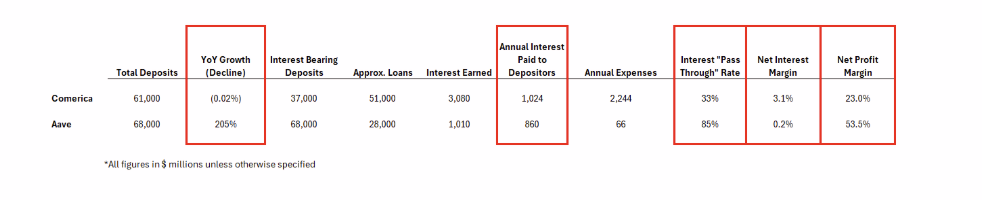

Let’s start with a quick refresher on the business model of banks. At their core, commercial banks essentially serve as middlemen providing capital re-allocation services: taking short-term demand deposits from customers and then lending that capital out to others in the form of (often longer-dated) loans. Banks receive loan repayments from borrowers and pass through a portion of those payments to depositors in the form of interest, while capturing the spread (“net interest margin”) on those two amounts. They may also invest in securities (e.g. US treasuries or mortgage-backed securities) as well. Net interest margins for US commercial banks are typically somewhere around 3-4%. For example, Comerica’s NIM in 2Q 2025 was 3.18%, generated from $70B in total earning assets ($60B in deposits) – or $575M in net interest income from $931M in earned interest less $356M in interest payments. To fund operations, Comerica had $561M in non-interest expenses in 2Q, resulting in $187M net income to shareholders (they generated an additional $274M in non-interest income, largely from various fees like card fees and service charges on checking accounts).

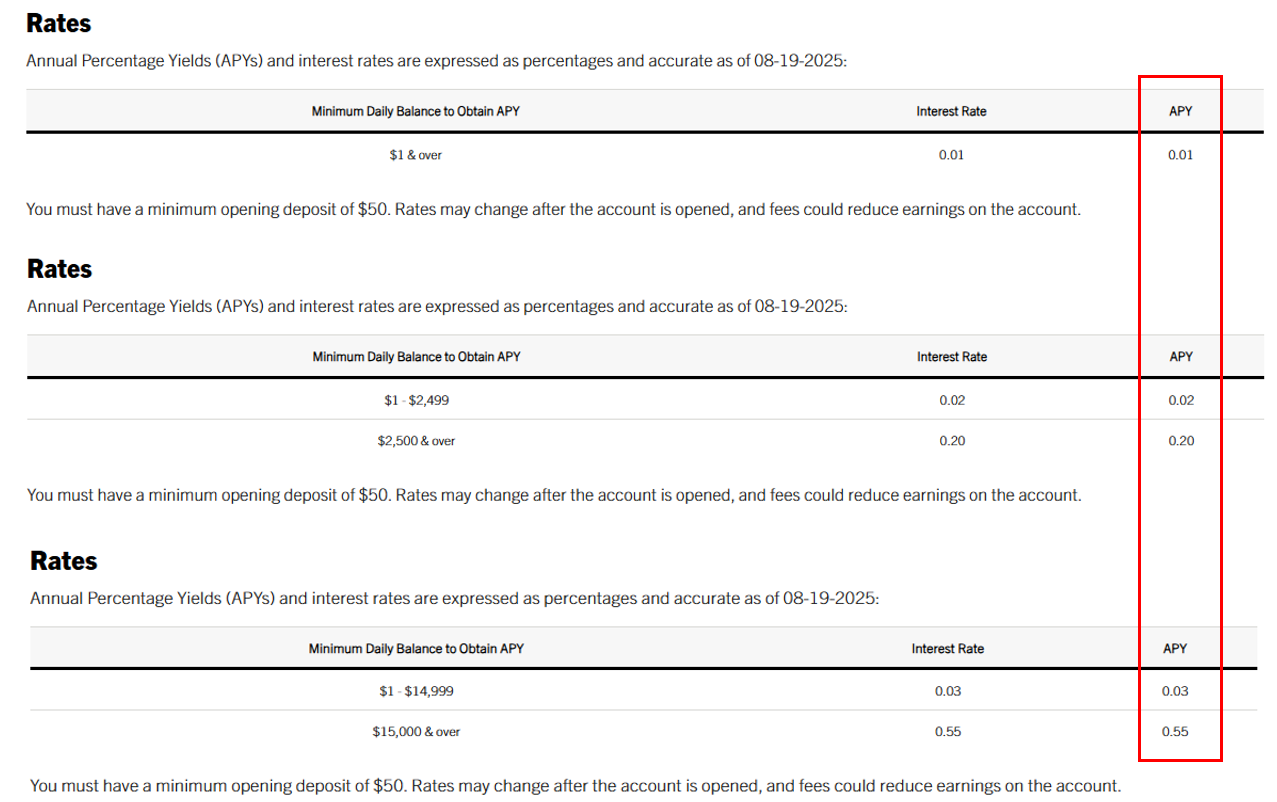

Because of this model, banks are structurally incentivized to pay as little as possible to depositors in the form of interest while earning as much as possible from the loans they make and the additional fees they can charge customers for their services. Checking accounts offer zero interest to depositors, and savings accounts might as well offer zero given how paltry most rates are in the current environment. Below are Comerica’s three types of savings and money market accounts – not exactly a great place to park cash, especially when inflation remains at elevated levels. For Comerica, $23B of their $60B deposits are non-interest bearing, and $37B of deposits are in interest bearing accounts. That is, depositors in aggregate are earning interest on just ~60% of their funds provided to Comerica.

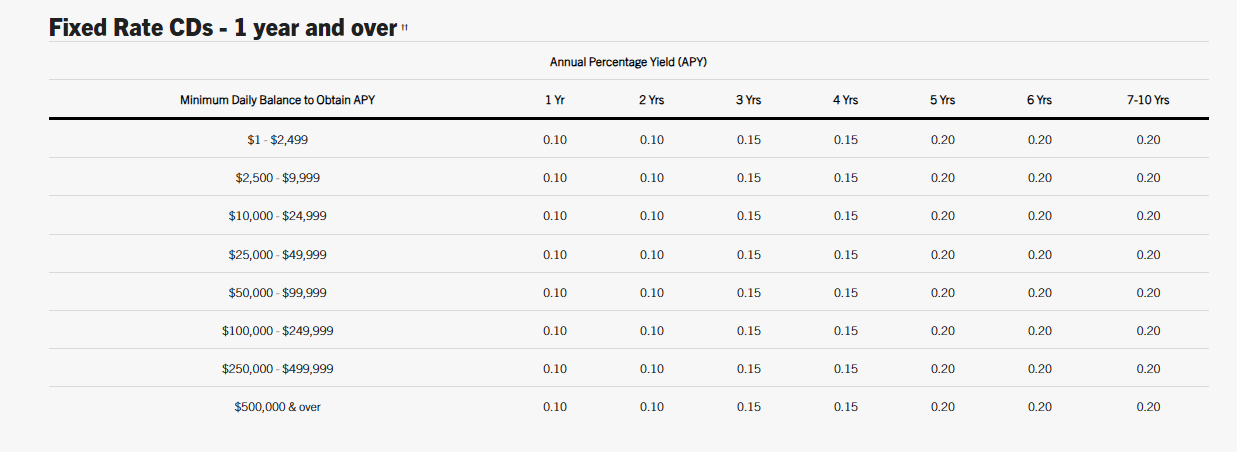

Now, one can always reach for ‘yield’ if they choose and agree to lock up their funds with Comerica for fixed time deposits (e.g. CDs). But even then, the interest offered is abysmal for the duration of these CDs, especially given the opportunity cost of that locked capital:

And this is undoubtedly a successful business. Though by no means one of the biggest banks in the US, dwarfed by institutions such as JP Morgan and Bank of America ($3.8T and $2.7T in assets, respectively), it is fair to say that Comerica is a large bank, ranking as the #34 largest in the US. It was founded in 1849, went public in 1991, is currently valued by the market at $8.7B, and employs roughly 8,000 people in 430 branches across the country. It is also of sufficient size and profitability to put its name on professional sports stadiums: the MLB’s Detroit Tigers play out of Comerica Park.

Okay, why the random tangent on banking and Comerica?

Simply because most would likely be surprised to learn that Aave – a decentralized, onchain lending protocol – is of a similar size as Comerica, and arguably, offers are far more fair and higher quality product than most regular commercials banks do today, all through a set of smart contracts on the internet, no branch in sight.

Aave – the DeFi Behemoth

Aave is one of the original lending protocols in the Ethereum ecosystem and is by far the largest in the vertical. In short, Aave provides a set of non-custodial smart contracts that allows anyone in the world to permissionlessly lend or borrow various cryptocurrencies without the need for any intermediaries. The vast majority of activity is driven by users borrowing against major blue-chip assets such as BTC and ETH, most often taking those loans out in stablecoins such as USDC or USDT. Loans are all open-ended, meaning there are no fixed repayment periods. Instead, interest rates are driven entirely by market supply and demand – if there is low borrowing activity, rates automatically adjust down, and in periods of heightened demand, rates automatically adjust higher. This ensures that depositors are always earning the fair rate on their supplied assets. In practice, depositors pool assets and borrowers can pull from that pool in exchange for interest payments, up to a programmatic limit based on their available collateral. Should a borrower’s collateral fall below the specified level, their collateral assets are automatically liquidated by smart contracts, protecting depositors. All interest payments are split pro rata to all depositors in a specific pool. As such, higher demands for certain assets results in higher interest payments to all depositors equally.

Aave recently hit an all-time intraday high of over $70B in assets in its contracts ($10B more deposits that Comerica), nearly $30B of which was borrowed at the time of writing. From that activity, Aave is currently generating over $1B in annual fees from borrowers, of which roughly 85% is passed through to depositors. There are other small channels through which Aave generates fees, such as fees on loans of just a few seconds known as flash loans, liquidation fees and borrower penalty fees, but these are small. From this, Aave is generating $140M in revenue that goes to the protocol – and importantly, pays out $860M to depositors. Compare that to Comerica, which generates $770M in quarterly interest revenue on the loans they make, but only pays $256M to depositors. If we very simply annualize those for Comerica, that works out to roughly $1B interest paid from $3B in interest generated from lending. These business models result in very different profit profiles, as one can see in the image below. Aave has annual expenses of $66M – of which $38.5M is dedicated to marketing and growth. It also has a protocol treasury of $236M.

It is important to remember that blockchain lending protocols, with their current designs, are optimized for lending/borrowing for similar, short durations. That is, essentially every market is a short term/on-demand market; there are no locked deposits or term loans involved. These are not designed for maturity transformation – that is, taking short term deposits to fund fixed long-term loans. Instead, every single deposit can be withdrawn at any time, and any loan can be repaid at any time. Aave does not make any mortgage loans, commercial loans or real estate constructions loans; it simply just provides overcollateralized consumer loans.

In practice, users are currently earning 4.6-5.5% on their USD stablecoins (USDC and USDT, respectively) and 4.9% on Euro stablecoins (EURC) – deposits with instant, on-demand liquidity. Ethena’s USDe dollar-pegged asset is currently yielding depositors 13% (largely due to the strong market demand for its staked and Pendle-fied versions).

Because of these differences, most current iterations of onchain lending protocols are highly complementary to more ‘traditional’ banks from a macro perspective in developed markets. However, for many retail users, the higher yield nature of these protocols may prove to be far more attractive than one’s normal checking or savings account at a bank, especially as distribution and abstraction simplify the user experience.

Obviously, there are also unique risks that arise here: there is still some regulatory uncertainty around these, and smart contract risk is always a spectre in the background of these new systems (though Aave itself has never been exploited – it is one of the most battle-tested protocols in the world). Further, there is naturally no Federal Government/FDIC guarantee on these deposits. But for the vast majority of people in the world that do not have access to US-dollar bank accounts or the ability to earn yield on their USD savings balances, internet-native protocols like Aave are game changing. Increasingly we are seeing debit and credit cards tied directly to user’s deposited balances in protocols such as these (EtherFi, Euler, Moonwell are but a few examples), allowing users to spend balances or access collateralized lines of credit via these lending protocols with full payment functionality through Visa and Mastercard networks globally.

Aave is not alone

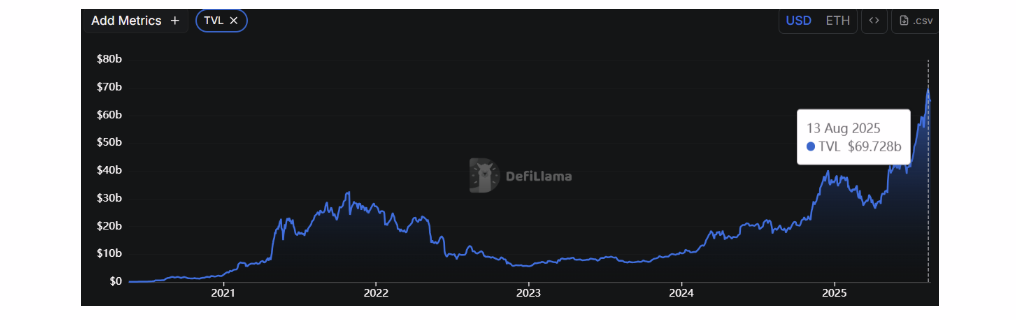

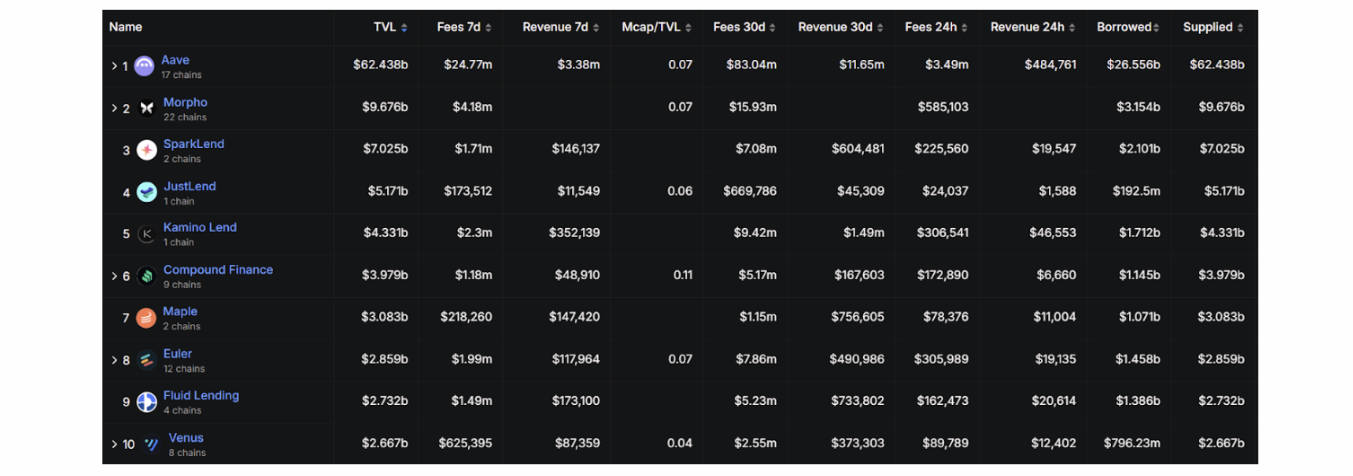

While Aave is by far the largest of these lending protocols, there are roughly 50 with over $50M in assets that offer similar capabilities but with their own unique differences that make them better suited for different use cases. And if we broaden the scope, there are over 500 different lending protocols, but many are likely no longer active, or are simply forks of the larger protocols with de minimis value in their contracts. In total, there is nearly $120B of assets across these protocols, generating over $40M per day in interest, or over $2B annually. As one can see in the chart below, these numbers are going parabolic, and as the base layer assets such as BTC, ETH and SOL continue to rise, so too will the available capital in these protocols and the resultant yields they are able to generate for depositors.

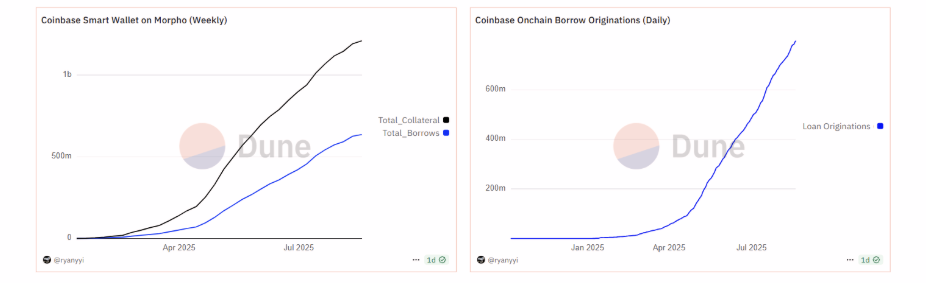

Morpho, Kamino, Compound and Euler are all designed around similar tenets as Aave: collateralized, permissionless lending. Each put their own spin on their functionality to better serve different use cases. Morpho and Euler, for example, take far more modular approaches to their protocol designs, enabling their protocols to support a far longer tail of tokens, compared to a relatively narrow set on Aave. Both are fast-growing alternatives to Aave and are highly competitive across a range of Ethereum Virtual Machine-based chains such as Ethereum, Base, Avalanche and Unichain. Coinbase, the largest US exchange, uses Morpho as the backend for its BTC-lending product, a sign of what is to come with so- called ‘DeFi mullet’ integrations: centralized exchanges and fintechs on the frontend tapping into decentralized protocols on the backend. There is over $1.2B deposited in this product, facilitating $640M in active loans currently outstanding (there has been $800M in total loans originated though this channel, almost entirely since the start of 2Q 2025). Morpho’s current market cap is $730M and Euler’s is just $190M.

Kamino takes a similar modular approach to design and risk as Euler and Morpho but is solely focused on the Solana ecosystem. Though there are other protocols on Solana that offer competitive services, Kamino has emerged as the clear front runner for SVM lending protocols and has grown to over $4B in assets, generating ~$20M in annual revenue at its current pace. Kamino’s team all have extensive Wall Street experience and employ PhDs to manage protocol risk. The circulating market cap of Kamino is $150M.

Other protocols on the list above such as SparkLend and Maple have slightly different models. Spark is technically an offshoot of the Sky stablecoin protocol and as such is highly synergistic to Sky’s model. Here, Sky allows users to deposit various assets into its contracts and in return mint Sky’s USD stablecoin, USDS. Sky has roughly $6B in TVL deposited currently. Sky delegates those funds to Spark to manage onchain, who then supplies liquidity to various onchain protocols to earn yield. This relationship is somewhat analogous to a central bank<>commercial bank relationship. That generated yield is then passed back to holders of USDS, who are able to earn DeFi yields on their stablecoin holdings, typically to the tune of 5-8%. There is now a new sub-DAO similar to Spark that will be focused on offchain lending to institutional partners. This sub-DAO is called Grove and it is working with institutions such as Janus Henderson and Appollo to build onchain yield products. Spark is trading at $120M market cap while SKY is valued at $1.5B off of $190M in net profits annually (e.g. trading at 8 P/E).

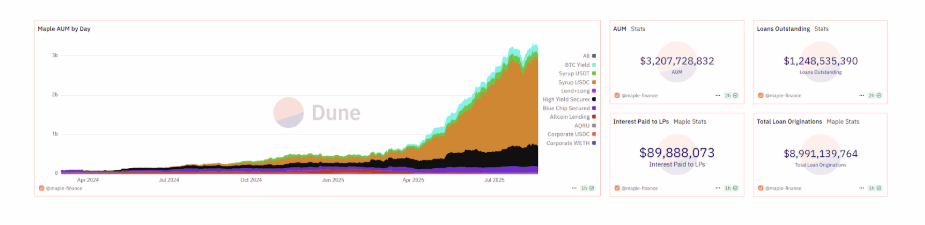

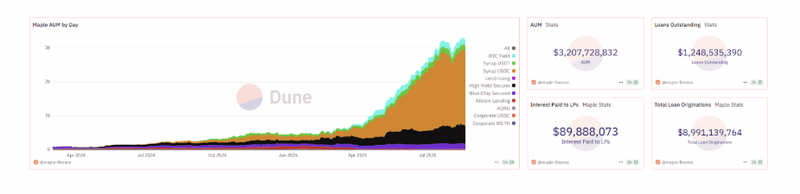

We have covered Maple a few times in the past, but they take what is colloquially referred to as a ‘CeDeFi’ approach, meaning that they largely act as an interface between onchain decentralized finance and offchain centralized finance. Primarily, Maple sources capital from onchain markets by having users deposit USDC or USDT into its smart contracts. In return, those users receive Maple’s own yield-bearing token called syrupUSD. With the deposited capital, Maple provides overcollateralized loans to institutional borrowers (Maple works with firms such as Bitwise and Cantor Fitzgerald). As those loans are repaid, Maple takes a small piece of the repayments and passes through the remainder to syrupUSD holders as yield. syrupUSD is currently yielding 7% for holders, and Maple’s asset base is now $3.2B, up from just $450M in January, resulting in ~$20M annual revenues to the protocol at current levels, of which 25% are directed towards buying back the SYRUP governance token off the open market.

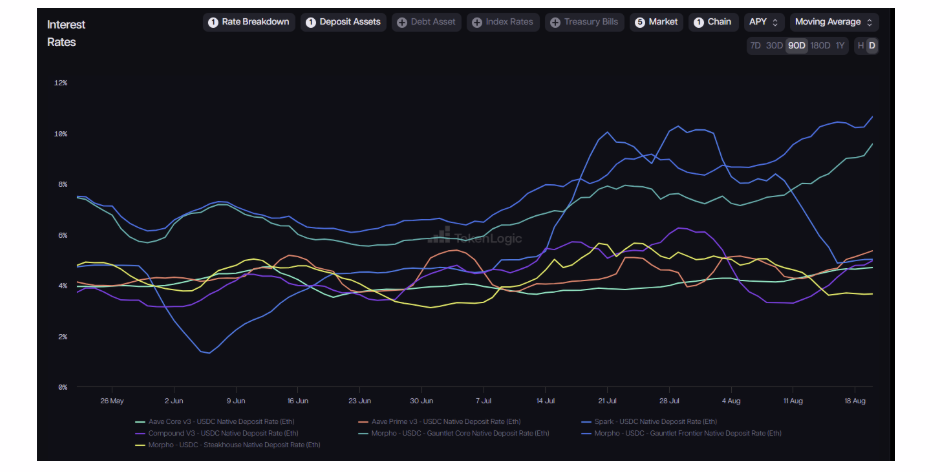

Below shows the rates that users are able to earn by depositing their stablecoins (e.g. USDC) into several of the above-mentioned lending protocols. As one can see, the rates available are quite attractive for instruments that have immediate on-demand liquidity and are derived from overcollateralized loans. Currently, it is pretty much table stakes to have your onchain ‘cash’ earning you 5-10%.

Growth has been vertical, and is likely to remain strong

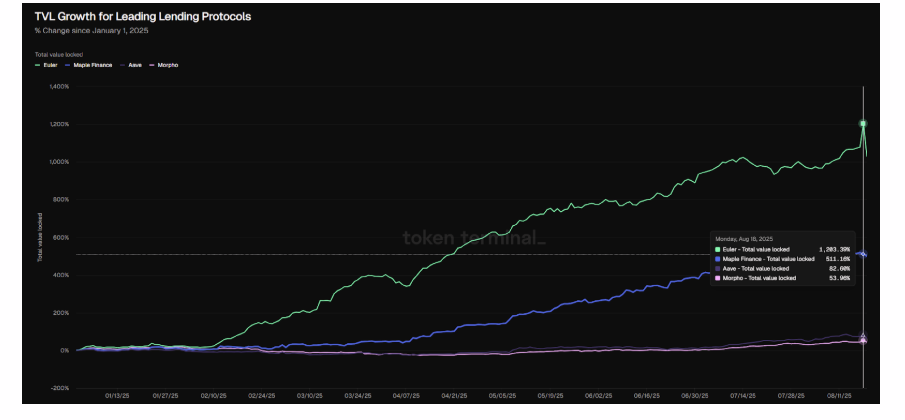

Each of the above-mentioned protocols are serious, investable businesses. All value of each accrues to the onchain governance tokens, there are no equity cap tables or shareholders in the traditional sense; governance oversight and value go to permissionless tokens circulating on these chains. Morpho and Aave have grown assets at a ‘slow’ pace of 50-60% over the past 8 months, collectively adding $35B between the two of them. Meanwhile, Euler and Maple have seen explosive growth, notching 1,000% and 500% growth since January. As blockchain technology is more widely adopted by companies and institutions around the world, and as the ongoing regulatory clouds start to clear (e.g. GENIUS and CLARITY legislation in the U.S.), we expect these leaders to continue to compound user and asset growth into the future. Aave has a clear shot of crossing $100B in assets in short order given its growth, which would put it comfortably in the top 30 of all US banking institutions, meanwhile Euler, Maple and Morpho are all likely to boast ‘balance sheets’ in the $10s of billions.

And who knows, a ballpark or two around the country might start to look a little different sooner than you think:

On rare occasions, we publish our highest-conviction investments. This week, Triton initiated a position in Hypercall (SYN). Our view: the market is pricing its past, while overlooking Hypercall's potential as a leading on-chain options platform.

Triton fully exited liquid assets by June 3 as macro pressure, ETF outflows, weak market structure, and capital rotation turned crypto risk-reward negative. The decision was not driven by broken fundamentals, but by a market where downside risk outweighed upside until clearer re-entry signals emerge.

We see Q1 2026 as a rare asymmetric crypto entry point—fundamentals are intact, valuations reset, and sentiment is at multi-year lows—positioning our long-horizon capital to capture potential outsized returns through our vertical-focused, data-driven approach.