Disclaimer: This is not financial advice. Anything stated in this article is for informational purposes only and should not be relied upon as a basis for investment decisions. Triton may maintain positions in any of the assets or projects discussed on this website.

TL;DR

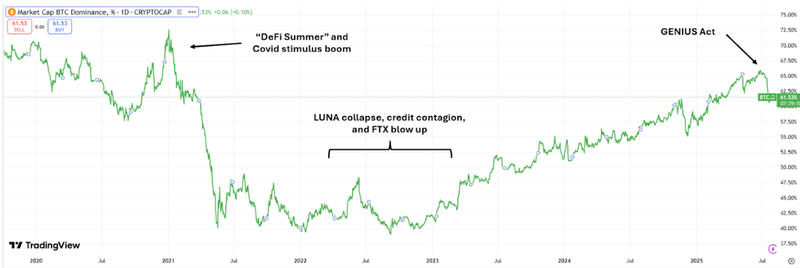

The End of Bitcoin Dominance?

Bitcoin has meaningfully outperformed ‘altcoins’ since 2023. To most investors, that much is clear and as a result, many have internalized Bitcoin as the default benchmark against which to compare all other digital asset performance. There are myriad reasons for this - some structural, some ephemeral - as we will explore in this post. But with the continued maturation of the industry and the arrival of long sought after legislation in the US, there are many reasons to believe that we are in the midst of a substantial sea change; one that is defined by the requisite conditions finally being in place for non-BTC digital assets to have their time in the sun. While this is a longer-term thesis, there are already early signs that this will be the case.

BTC.D has been up-only

A simple metric to measure the relative growth of Bitcoin against the rest of the digital asset market is known as Bitcoin dominance (BTC.D). In short, it divides Bitcoin’s market cap against that of the entire industry. The chart below makes it abundantly clear that BTC.D growth has been the clear trend since late 2022. Why has this been the case? Primarily two reasons, the second of which is arguably derivative of the first: 1) BTC is unique as a digital store of value and macro hedge asset, and 2) the regulatory regime around BTC has been far more clear, for much longer, than for any other digital asset. Let’s unpack those.

As we detailed in depth in our piece, “Digital Gold”, BTC is unique in its position as a scarcity-focused, fully decentralized asset that, ironically, has benefited greatly from its lack of cash flows and thus lack of ‘intrinsic value’ in the traditional sense. In short, it is the internet age’s best representation of a true digital non-sovereign store of value. Because of this, as the viability and staying power of the underlying technology and code has been proven over time, investors have gradually accepted Bitcoin as a decorrelated asset that is increasingly turned to in times of global uncertainty or heightened monetary debasement, as we have seen over the past few years. Across retail investors, high net worth investors, family offices and ‘traditional’ hedge funds, BTC is now held as a hedge asset in addition to a speculative one. Now, companies and larger institutional investors such as sovereign/state funds, pensions and endowments are starting to build BTC allocations into their portfolio construction.

Bitcoin is very unique in this role among digital assets - essentially every other coin or token is far more akin to a tech company. Some are far more mature (such as Ethereum), but the vast majority should be viewed in the same manner as a startup. That is, though they are often put in the same general ‘crypto’ bucket, the value drivers of $2 trillion BTC and a $2 billion stablecoin protocol are substantially different, let alone a 6-month-old, $50M onchain perps DEX. There is undoubtedly a heavy BTC-beta factor at play for these given some structural dynamics and the general view of the market, but there are also far more idiosyncratic factors at work that can lead to out- or under-performance against BTC, and we expect these to play a more significant role going forward. Increasingly, these factors are starting to shift more in favor of non-BTC digital assets, as we’ll explore a little later.

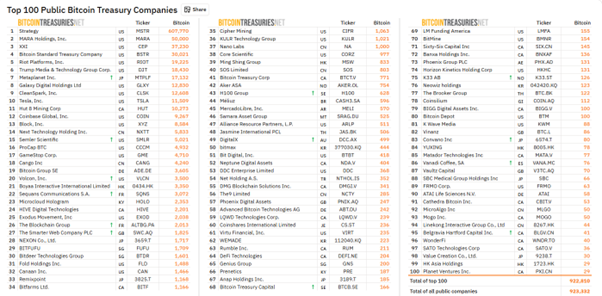

Because of this far simpler structure (e.g. no cash flow, no ‘intrinsic value’, no issuer), Bitcoin also was given a far more clear regulatory treatment than was any other digital asset. Case in point: Bitcoin was first explicitly classified as a commodity by the CFTC in 2015. Because of that, there has been relatively little regulatory overhang clouding Bitcoin; professional US investors have had the greenlight to underwrite and invest in Bitcoin for almost a decade. Because of this head start, a far more robust ecosystem has also developed around BTC that is now (e.g. in the past 3 months) beginning to form for Ethereum (the 2nd largest digital asset) and others. For example, Strategy (formerly Microstrategy) has been a major driving force behind BTC, effectively running a non-stop TWAP in the market, insensitive to price. To date, they have accumulated over 3% of all circulating supply, and there are dozens of copy cats around the world mimicking this strategy, such as Metaplanet in Japan, as well as regular operating companies that have elected to hold BTC, such as Tesla. The list of companies holding BTC is long:

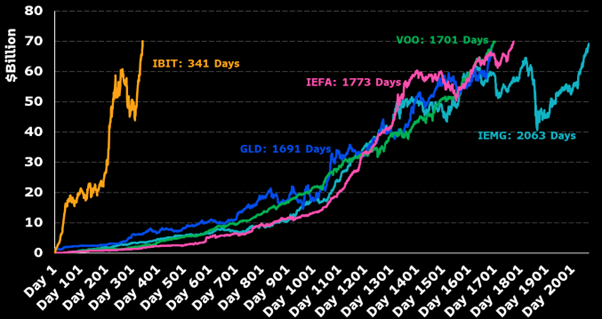

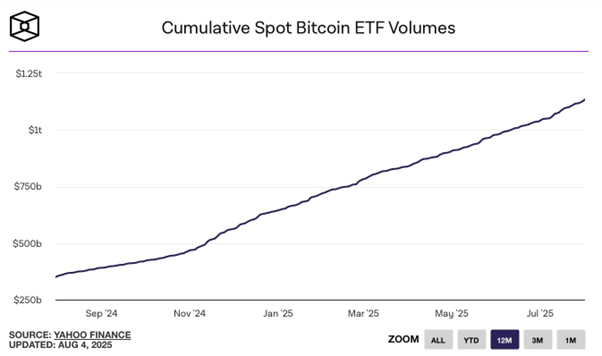

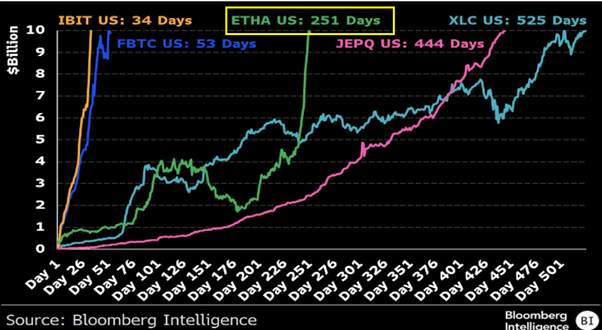

Similarly, ETFs enabled institutions and retail buyers to access Bitcoin easily through their brokerages with best-in-class distribution (e.g. Blackrock), avoiding the need to worry about self-custody, wallets, and all the frictions associated with purchasing digital assets directly. When the BTC ETFs went live in January 2024, the floodgates to new capital exploded open: Blackrock’s IBIT is single best performing ETF in history by just about any measure and represents over half of the ~6.5% of all BTC that these now hold ($150 billion). The chart below from Bloomberg shows the comparative times it took IBIT to hit $70 billion in net new inflows relative to the previous 4 fastest ETFs:

In comparison, the SEC was still unclear about whether they deemed ETH (the 2nd largest digital asset, ~$400B) as a commodity or security until summer 2024 when they surprised the market by approving spot ETH ETFs, which the market took to implicitly mean ETH too was seen as a commodity. Even then, SEC Chair Gensler frequently equivocated on ETH’s status, and it was not until just this year that the first unequivocal specification of ETH as a commodity was made by the SEC. Keep in mind, throughout much of the last political campaign cycle in the US, prominent Senators (e.g. Warren, Brown) ran entire campaigns around building ‘anti-crypto armies’. In short, the legal standing of digital assets outside of Bitcoin in the US has very much been in flux until just a few months ago. We detailed this confusing regulatory landscape in a newsletter post earlier this summer. This contemporaneous quote from global law firm Baker Mackenzie sums up the inconsistency well:

All this has meant that the true capital inflows into non-BTC assets have been hamstrung to date. Investors in the largest capital market in the world (US) have been unclear about the rules of the game and thus hesitant to invest. Further, teams building in the space have been terrified to do it in the US, pushing builders offshore and out of the US capital market and tech centers, while simultaneously sidelining most US retail investors, and importantly, consumers – the actual users of the products. Complicating this, it also has led many to design entirely convoluted governance structures and obscure tokenomics that make investing in tokens a mine field, nearly impossible to do for anyone but a full-time investor in the space.

But don’t take your author’s word for it. Paul Atkins, the new Chair of the SEC happened to deliver this speech just last week, and it is nothing short of exceptional in terms of what it means for digital asset adoption in the US. Here’s one section:

These dynamics all cascade down to every digital asset that a) is often denominated in native blockchain tokens such as ETH, SOL etc. and are reliant on those ecosystems thriving – e.g. far more sensitive beta to ETH and SOL than BTC, and b) that have similarly historically been unclear as to how they are treated by regulators and thus largely uninvestable. It is simply structural: the cost of capital skyrockets for a startup when investors have no clarity as to whether that company is going to be sued by the SEC next month or on what grounds, and founders are hesitant to get involved in the first place.

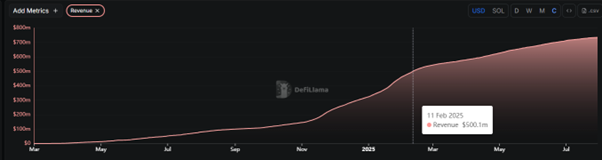

There is also a major lemon problem that the lack of regulatory clarity has helped create – and that is why, as investors, we are so optimistic about the SEC’s current direction. Simply, most people have heard of the TRUMP, LIBRA and MELANIA memecoins, or of Terra/LUNA and FTX, because projects like these are what frequently dominate headlines. At the same time, one can confidently say that very few understand that Aave is a top 40 bank in terms of assets in the US, or that Pump.fun and Hyperliquid are actually the fastest companies to earn $500M revenue in the world, not Wiz, OpenAI, Anthropic or any of the other Cloud or AI companies dominating the headlines.

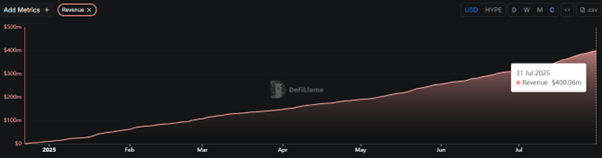

The margins are also simply unheard of in many cases: Tether is as profitable with just 100 employees as Goldman Sachs is with its 40,000 employees ($13B vs $14B net income in 2024, respectfully – in fact Tether just announced net profits of $4.9B this past quarter), and Hyperliquid operates with a net margin of 93% with 100% of those profits directed towards buying back the token from the market. Hyperliquid is currently generating over $1B in annual run rate. Unfortunately, the caution and lack of attention paid is arguably justified given the track record of crypto and the ever-present perspective that all of crypto is illegal or is not sustainable. But in a very practical sense, it severely drives the cost and availability of capital up and some of the best businesses in the world are simply underfunded and overlooked. Even a few bad lemons are enough to ruin the whole batch for some (or most?) investors.

Importantly, this is now changing

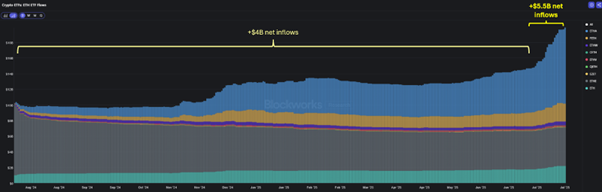

Since late 2024 and with the new administration in 2025, this has been changing. As we mentioned above, the surprise approval of ETH ETFs in July 2024 severely caught the market off guard. And whereas the BTC ETFs benefitted from a long period to underwrite and establish sales channels and distribution before going live, none of that was in place for Ether ETFs before approval, and unlike Bitcoin that is a relatively simple asset, ETH is highly complex and far more difficult to understand. But with those channels now in place you are now starting to see the change in flows following all of the beneficial changes:

Beyond Ethereum, there are now new ETFs expected to launch for many more assets in the US, including Solana (the 2nd largest ecosystem chain) this year. One smaller vehicle is already live (REX-Osprey, $140M net inflows in first month live), but the big players are still coming: Blackrock has not yet filed for a SOL ETF, but every other major issuer of BTC and ETH ETFs, such as Fidelity, Bitwise and VanEck, are on board.

The Change Following US Regulations Has Been Rapid

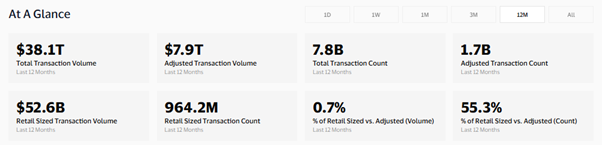

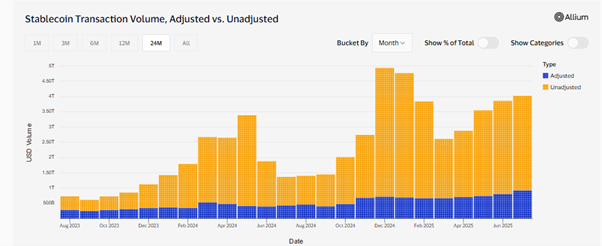

On July 18, the US signed into law the GENIUS Stablecoin bill that now officially creates a legal & regulatory framework for stablecoins in the US. Likely going into effect in early 2027, this legislation opens the door for every bank and financial institution and many tech companies to get involved. Just about every major player has either already signaled intent or is already heavily involved in stablecoins: JPMorgan, Citibank, Bank of America, Visa, Paypal, Stripe, Wells Fargo, Fidelity, Shopify, Robinhood, Interactive Brokers, and the list goes on. Perhaps more importantly, these companies are getting involved through public blockchains such as Ethereum, Solana and Base, rather than primarily relying on internal private ledgers. It is tough to estimate how big stablecoins can grow, but it is not a stretch to believe that we are talking trillions in supply and 100s of trillions in volume in short order – up from the current $250B and $38T, respectively (US Treasury Secretary Bessent’s own prediction is $3.7T in supply). Keep in mind that stablecoins are already competitive with Visa and Mastercard (combined $1.2 trillion market caps), and they’re not even “legal” in the US yet:

The amazing part is, even with all of the above said, the SEC and CFTC still do not agree as to who has jurisdiction over what, what the laws and requirements are for digital assets, or what legal frameworks need to be in place to regulate these in July 2025. When those in crypto point to lack of regulatory clarity, this is the primary issue. Thankfully, this too will finally be clarified in the upcoming CLARITY market structure legislation, expected to pass (perhaps) later this year or early 2026. Until this legislation is finalized, the lack of firm clarity is still preventing capital flows to the space, but the massive interest in Ether and ETF flows and wild success of USDC stablecoin issuer Circle’s IPO suggest investors are positioning themselves now, and the early disclosures of what is likely to be in the legislation are allowing companies to start preparing well in advance.

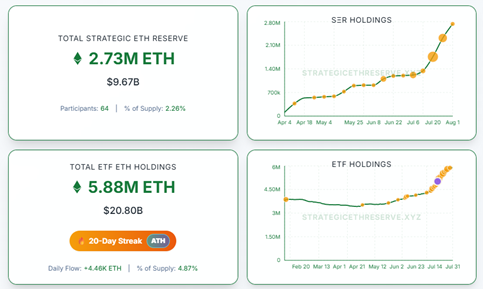

With this added clarity and legal structure (GENIUS bill, and what is likely to be included in CLARITY), builders and investors are far more willing to get involved. We mentioned earlier that there is a robust ecosystem around BTC, such as Strategy. Over the past few months, we started seeing similar vehicles pop up, not only for Ethereum and Solana, but for a wider range of “altcoins” as well, such as HYPE and SUI. For ETH, there have been multiple multi-billion dollar raises led by prominent figures such as Ethereum’s co-founder Joe Lubin and Fundstrat’s Tom Lee, each racing to acquire 5-10% of all circulating supply. Importantly, these are price-insensitive buyers with fiduciary mandates to maximize acquisition of the underlying assets (ETH, SOL, etc.), and in many cases, to also then deploy those assets into onchain DeFi protocols, rather than just simply buy and hold as Strategy does. As such, the relative impact of each dollar raised through these vehicles is likely to be far higher given the deployment of assets back into the economies, and due to the relative sizes of the raise against the circulating market caps of the underlying assets. That is, $5 billion raised to put to work on Solana ($100B market cap and then deployed into onchain lending and staking protocols) is far more impactful than $5 billion raised to put to work on Bitcoin ($2T market cap, simply bought and held).

Finally, this all means that the market is starting to mature. The transition from hyper-speculative retail led narrative trading – and the crazy boom busts crypto is known for - to long-term, fundamentals-focused professional investing is accelerating. Opportunities to invest in venture-stage liquid companies that are building in this exploding space are increasing, and the structural SAMs/TAMs continue to expand as regulation and worldwide adoption improves. The underlying strength of onchain businesses has never been higher: active users, use cases, volumes, revenue generation are all seeing hockey-stick growth, and with the full-throated endorsement and adoption of the industry in the US, it is fair to say that the future is going to look far, far different than the past.

On rare occasions, we publish our highest-conviction investments. This week, Triton initiated a position in Hypercall (SYN). Our view: the market is pricing its past, while overlooking Hypercall's potential as a leading on-chain options platform.

Triton fully exited liquid assets by June 3 as macro pressure, ETF outflows, weak market structure, and capital rotation turned crypto risk-reward negative. The decision was not driven by broken fundamentals, but by a market where downside risk outweighed upside until clearer re-entry signals emerge.

We see Q1 2026 as a rare asymmetric crypto entry point—fundamentals are intact, valuations reset, and sentiment is at multi-year lows—positioning our long-horizon capital to capture potential outsized returns through our vertical-focused, data-driven approach.